Parker-Hannifin Corp Stock (PH) Closed Up by 3.05% on Jun 25: Facts Behind the Movement

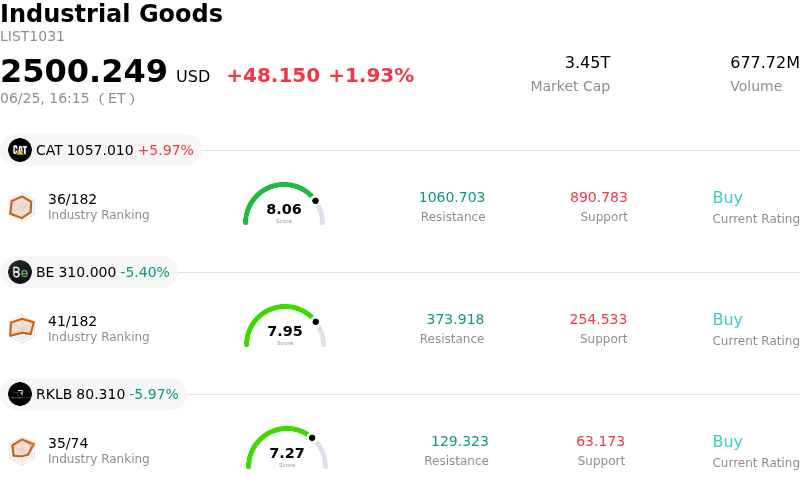

Parker-Hannifin Corp (PH) closed up by 3.05%. The Industrial Goods sector is up by 1.93%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Caterpillar Inc (CAT) up 5.97%; Bloom Energy Corp (BE) down 5.40%; Rocket Lab USA Inc (RKLB) down 5.97%.

What is driving Parker-Hannifin Corp (PH)’s stock price up today?

Parker-Hannifin Corporation experienced a notable upward movement on Thursday, accompanied by significant intraday volatility. The stock benefited from a favorable combination of broader macroeconomic trends, sector rotation, and strong company-specific fundamentals that attracted institutional capital seeking stable, high-quality industrial compounders.

The primary macro catalyst driving the upward momentum was a positive shift in market sentiment following the release of key inflation metrics. The personal consumption expenditures price index reported inflation levels that were in line with consensus expectations, while the monthly figure came in slightly below forecasts. This brought considerable relief to the market, helping to ease Treasury yields and lower interest rate concerns. As capital costs stabilize, capital-intensive industrial giants like Parker-Hannifin naturally see improved financial outlooks, boosting their attractiveness.

Additionally, a significant drop in global crude oil prices acted as a vital tailwind. Lower energy and transportation costs directly benefit industrial manufacturers by easing supply chain and raw material expenses. With energy pressures fading, investors actively rotated capital out of highly valued mega-cap technology names and into high-performing cyclical sectors, particularly industrials. The broader industrials sector paced the market's gains as a result of this rotation, lifting Parker-Hannifin.

At the company level, the stock's rise builds upon a strong fundamental narrative that has steadily gained traction among institutional investors. Confidence remains high following the company’s recent decision to raise its quarterly cash dividend, extending its historic track record of annual payout increases to seven consecutive decades. This commitment to returning cash to shareholders, combined with a record-high backlog in its high-margin Aerospace Systems segment, underscores the durability of its cash flow.

Furthermore, long-term investors are highly optimistic about Parker-Hannifin's pending acquisition of Filtration Group Corporation. This strategic multi-billion-dollar deal is expected to create one of the largest global industrial filtration platforms, significantly increasing the company's exposure to high-margin, recurring aftermarket revenue streams. Ratings agencies have also recently revised their outlooks on the company to positive, highlighting that strong consistent cash generation and operating performance should comfortably support the acquisition's integration while maintaining a robust balance sheet.

The intense intraday volatility observed during the session reflected a tug-of-war across the broader market. While blowout earnings in the semiconductor sector initially triggered a broad rally, subsequent price hikes from major consumer tech giants injected uncertainty, causing sudden swings in the major indices. In this volatile environment, Parker-Hannifin emerged as a highly favored defensive growth play. Investors sought refuge in high-quality industrial leaders with robust backlogs, predictable aftermarket revenue, and proven capital deployment strategies, driving the stock higher on the day.

Technical Analysis of Parker-Hannifin Corp (PH)

Technically, Parker-Hannifin Corp (PH) shows a MACD (12,26,9) value of 19.608, indicating a buy signal. The RSI at 65.943 suggests neutral condition and the Williams %R at 10.541 suggests overbought condition. Please monitor closely.

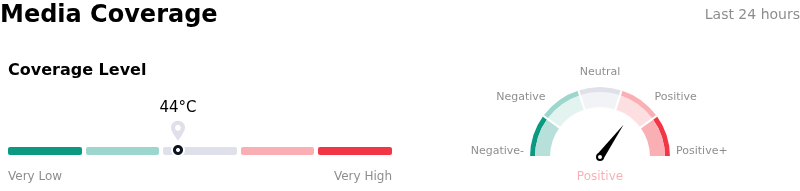

Media Coverage of Parker-Hannifin Corp (PH)

In terms of media coverage, Parker-Hannifin Corp (PH) shows a coverage score of 44, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Parker-Hannifin Corp (PH)

Parker-Hannifin Corp (PH) is in the Industrial Goods industry. Its latest annual revenue is $19.85B, ranking 9 in the industry. The net profit is $3.53B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1027.57, a high of $1147.00, and a low of $682.12.

More details about Parker-Hannifin Corp (PH)

Company Specific Risks:

- Premium Valuation and Downside Vulnerability: Discounted cash flow (DCF) analyses updated on June 23–24, 2026, indicate that the stock's trading price of approximately $948–$962 represents an estimated 21.5% to 29% premium over its intrinsic value range of $598–$744. With a trailing P/E multiple of roughly 35x—significantly higher than the machinery industry average of 26.8x—the stock is highly susceptible to contraction on any guidance or growth disappointments.

- Slowing Industrial End Markets and Escalating Capital Needs: Analyst reports from June 24, 2026, point to a growing near-term tension between slowing industrial end-market demand and the company's elevated capital expenditures (CapEx). High CapEx and expensive restructuring plans represent a primary risk to the preservation of operating margins and cash flow durability in the short term.

- Severe Integration and Leverage Risks from Large M&A: S&P Global Ratings and market commentators highlighted risks surrounding the massive pending $9.25 billion acquisition of Filtration Group Corporation. Integrating a transaction of this scale introduces substantial operational execution risk, and the added debt burden is projected by S&P to increase the company's leverage up to 3x, compressing financial flexibility.

- Insider Divestments and Profit-Taking: Investor updates published on June 24, 2026, brought attention to significant insider selling over the past twelve months, including a $3.2 million stock sale by the President and COO at levels below current market prices. This heavy insider divestment is interpreted by some institutional analysts as a signal that executive leadership believes the stock has reached a full or premium valuation.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.