Arm Holdings PLC Stock (ARM) Moved Down by 4.11% on Jun 22: What Investors Need To Know

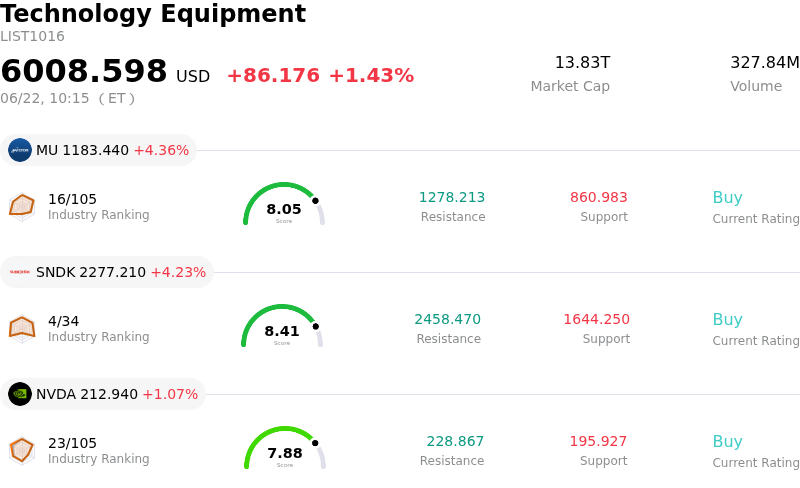

Arm Holdings PLC (ARM) moved down by 4.11%. The Technology Equipment sector is up by 1.43%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 4.36%; SanDisk Corporation (SNDK) up 4.23%; NVIDIA Corp (NVDA) up 1.17%.

What is driving Arm Holdings PLC (ARM)’s stock price down today?

The downward movement and heightened intraday volatility in Arm Holdings plc can be attributed to a combination of overstretched valuations, recent analyst downgrades, insider selling, and structural strategic shifts that have introduced execution risks.

A primary catalyst for the downward pressure is growing market anxiety over the company’s extreme valuation. Following a massive year-to-date rally fueled by the artificial intelligence boom, the stock's trailing price-to-earnings ratio surged to exceptionally high levels. This premium multiple has left the high-beta stock highly vulnerable to decompression, especially after the Federal Reserve's hawkish dot-plot update. The prospect of sustained higher interest rates has triggered broad profit-taking across high-valuation technology names, with the company facing the brunt of this sector-wide rotation.

Compounding this valuation pressure, New Street Research recently downgraded the stock from Buy to Neutral. The downgrade warned that the stock’s rapid run-up had pushed its price to an unsustainable premium relative to its intrinsic value. A discounted cash flow analysis published on the same day further highlighted concerns that the stock is trading significantly above its fundamental value, amplifying bearish sentiment among institutional and retail investors alike.

Operational and strategic uncertainties have also weighed on investor sentiment. The company’s strategic pivot into developing and selling its own custom proprietary hardware, including its new AGI CPU, has raised concerns about channel conflicts. Traditionally operating as a neutral, high-margin intellectual property licensor, the company now risks being viewed as a direct competitor by its primary licensing partners, such as Nvidia, Qualcomm, and Amazon Web Services. This friction threatens to disrupt the firm's core customer ecosystem. Furthermore, tight advanced-node foundry capacity continues to pose execution risks, potentially bottlenecking its ability to fulfill custom silicon orders on time.

Finally, recent market sentiment has been dampened by significant insider transactions. Multi-million dollar open-market share liquidations by senior executives, including the Chief Commercial Officer and Chief Accounting Officer, have triggered localized negative sentiment. These large-scale insider sales have led market participants to question the near-term upside potential of the stock, compounding the downward momentum and contributing to the day's sharp, volatile trading session.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of 5.879, indicating a buy signal. The RSI at 68.976 suggests neutral condition and the Williams %R at 8.580 suggests overbought condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $265.56, a high of $500.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- Institutional Analyst Downgrade and Extreme Valuation Premium: On June 18, 2026, New Street Research downgraded Arm Holdings from Buy to Neutral, warning that the stock's massive year-to-date rally has stretched its valuation to an unsustainable premium. With a trailing P/E ratio exceeding 490x, the company faces severe valuation compression risks and heightened intraday volatility following hawkish macroeconomic shifts.

- Ecosystem Friction and Channel Conflict: Arm's transition into selling its own proprietary silicon—specifically the new 136-core AGI CPU co-developed with Meta—creates a direct conflict of interest with its established customer base. Key licensing partners such as Nvidia, Qualcomm, Apple, and AWS may increasingly view Arm as a hardware competitor, threatening its core high-margin intellectual property licensing business model.

- Escalating Antitrust and Regulatory Investigations: The company faces intensifying regulatory headwinds, including an active U.S. Federal Trade Commission (FTC) probe. The regulator is examining whether Arm's push into physical chip manufacturing will lead it to illegally monopolize the market by refusing or degrading CPU blueprint licensing terms for rival hardware companies.

- Significant Executive Insider Share Liquidations: Market sentiment has been weighed down by multi-million dollar open-market share sales executed by senior executives. Recent filings disclose substantial liquidations in late May and June 2026 by the Chief Commercial Officer and Chief Accounting Officer, heightening investor concerns over peak valuation levels.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.