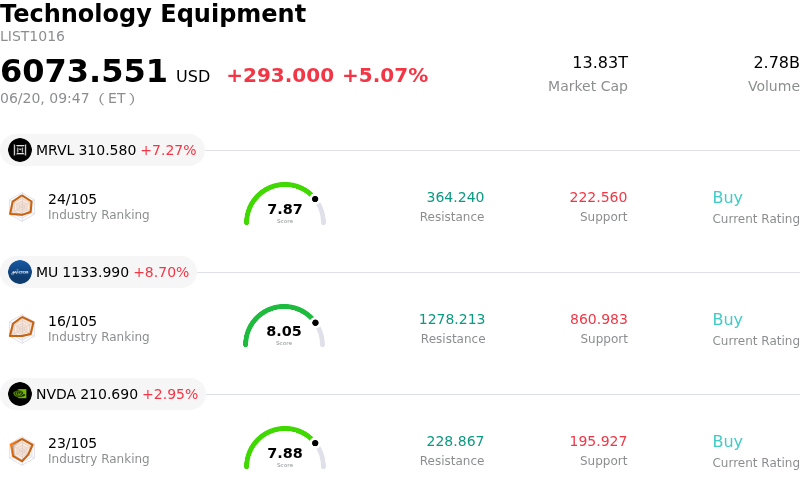

Micron Technology Inc Stock (MU) Opened Up by 8.70% on Jun 20: Drivers Behind the Movement

Micron Technology Inc (MU) opened up by 8.70%. The Technology Equipment sector is up by 5.07%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Marvell Technology Inc (MRVL) up 7.27%; Micron Technology Inc (MU) up 8.70%; NVIDIA Corp (NVDA) up 2.95%.

What is driving Micron Technology Inc (MU)’s stock price up today?

On the final trading session before the holiday weekend, Micron Technology experienced a substantial upward movement, driven by a convergence of bullish factors in the memory chip sector. The primary catalyst was a flurry of aggressive price-target upgrades from major Wall Street investment firms ahead of the company's upcoming third-quarter fiscal earnings report. Analysts from several prominent firms significantly raised their expectations, setting steeply upgraded price targets. This surge in institutional optimism is rooted in the belief that the current memory cycle has transitioned from a typical cyclical rebound into a structural, multi-year super-cycle.

Adding immense weight to the structural shortage thesis were recent remarks from Apple CEO Tim Cook. He indicated that price hikes in memory and storage chips have become unavoidable due to soaring demand, driven heavily by artificial intelligence applications. Because Apple is renowned as one of the tech industry’s largest and most stringent component buyers, this high-profile commentary served as strong external validation of the severe memory supply crunch. It confirmed that pricing power has firmly shifted back to memory manufacturers like Micron, as shortages begin to spill over from enterprise AI data centers into consumer devices like premium smartphones and personal computers.

The fundamental backing of this demand surge is further reinforced by Micron's highly coveted high-bandwidth memory, which is essential for powering next-generation artificial intelligence servers. Micron has already completely committed its entire high-bandwidth memory capacity for the calendar year under long-term customer agreements. Because this specialized memory requires significantly more manufacturing capacity per bit than standard dynamic random-access memory, it has effectively restricted global supply. The resulting contract price increases in both dynamic random-access memory and flash storage are expected to yield record-breaking profit margins and unprecedented cash flow for the semiconductor giant.

In addition to company-specific strength, broader semiconductor industry sentiment was lifted by geopolitical and domestic manufacturing developments. Reports of a strategic partnership between Apple and Intel to manufacture chips domestically in the United States ignited optimism across the entire domestic semiconductor supply chain. As the premier U.S.-based memory manufacturer, Micron stands to benefit directly from this momentum toward localized, high-tech manufacturing. While defensive hedging in the options market and high implied volatility signal near-term caution ahead of the earnings release, the combination of robust structural demand, soaring pricing power, and positive domestic industry developments has successfully catalyzed this latest surge.

Technical Analysis of Micron Technology Inc (MU)

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of 1.487, indicating a buy signal. The RSI at 66.392 suggests neutral condition and the Williams %R at 5.232 suggests overbought condition. Please monitor closely.

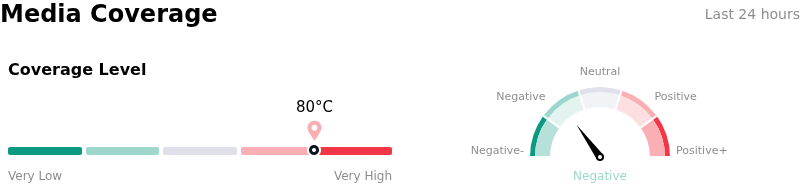

Media Coverage of Micron Technology Inc (MU)

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 80, indicating a high level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Micron Technology Inc (MU)

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $987.27, a high of $1750.00, and a low of $190.00.

More details about Micron Technology Inc (MU)

Company Specific Risks:

- Extreme Options Bearish Hedging and Implied Volatility Spikes: Ahead of Micron's critical Fiscal Q3 2026 earnings release on June 24, the options market is displaying heavy defensive positioning. Implied volatility (IV) has spiked to between 100% and 121%—nearly double its 52-week average—and the put-to-call open interest ratio has reached an extreme 10.28 for July post-earnings contracts, leaving the stock highly vulnerable to sharp downward corrections on any minor earnings or guidance miss.

- Synchronized Competitor CapEx and Overcapacity Downturn: To capture the artificial intelligence boom, Micron is pursuing a massive fiscal 2026 capital expenditure target exceeding $25 billion. However, synchronized, capital-intensive fab expansions by major rivals Samsung and SK Hynix risk flooding the market with excess next-gen 1c DRAM and HBM supply by 2027, threatening to trigger a classic cyclical oversupply downturn, erode average selling prices (ASPs), and contract gross margins.

- Premium Valuation and Heightened Macro Vulnerability: Following a rapid rally pushing the stock to approximately $1,134, Micron is trading at an elevated P/E ratio of 51.37x, suggesting a steep valuation premium with a minimal margin of safety. This leaves the stock highly sensitive to profit-taking and technical sell-offs (such as its 6.2% single-day drop on June 16, 2026), especially as recent hawkish economic projections from the Federal Reserve indicate that borrowing costs will remain higher for longer in 2026.

- Unprecedented Execution Hurdles and Pricing-Power Debates: While Micron's 2026 high-bandwidth memory (HBM) supply is fully contracted, analysts are deeply divided on the sustainability of the current cycle. Any cautious management commentary next week regarding future memory pricing, a slowdown in enterprise AI capital spending, or a failure to lock in long-term strategic customer commitments past 2026 would rapidly invalidate Wall Street's aggressive price target increases and trigger deep peak-to-trough drawdowns.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.