Accenture PLC Stock (ACN) Moved Down by 17.99% on Jun 19: Key Drivers Unveiled

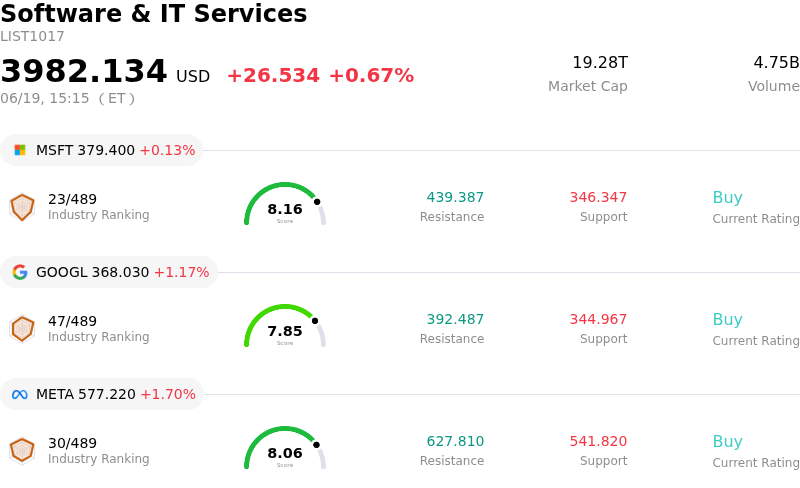

Accenture PLC (ACN) moved down by 17.99%. The Software & IT Services sector is up by 0.67%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) up 0.13%; Alphabet Inc Class A (GOOGL) up 1.17%; Meta Platforms Inc (META) up 1.70%.

What is driving Accenture PLC (ACN)’s stock price down today?

Accenture experienced a severe downward adjustment in its share price following the release of its third-quarter fiscal 2026 financial results, which triggered intense selling pressure and record intraday volatility. The primary driver of the bearish sentiment was a combination of top-line revenue missing consensus expectations, a contraction in new bookings, and a downward revision of full-year growth guidance.

While Accenture’s diluted earnings per share beat Wall Street forecasts, the top-line softness pointed to systemic challenges in client spending. New bookings for the quarter declined compared to the prior-year period, reflecting a broader pullback in discretionary consulting budgets as enterprise clients remain highly cautious amid macroeconomic uncertainty.

The most significant catalyst for the downward pressure was management's revised business outlook. Accenture trimmed its full-year fiscal 2026 revenue growth forecast, lowering the upper bound of its previously guided range. Management highlighted severe headwinds within its U.S. federal government business segment, citing slower procurement cycles and a wave of contract reviews that are dragging down overall growth. This confirmed fears that the growth trajectory projected by management earlier in the year is no longer achievable.

Adding to investor anxiety was the company's aggressive capital reallocation strategy announced alongside the earnings release. Accenture unveiled plans to spend billions to acquire several operational technology cybersecurity firms, including Dragos, runZero, and NetRise. While management framed these transactions as a strategic expansion into physical-process security in the age of artificial intelligence, many investors reacted with skepticism. The market expressed concern over the high cost of these acquisitions at a time when the company's core organic consulting business is decelerating.

Wall Street analysts responded to the earnings report and revised guidance with a wave of price target cuts and downgrades. Many noted that the anticipated monetization of artificial intelligence projects has not materialized quickly enough to offset the broader slowdown in traditional software and consulting services. The alignment of a trimmed corporate outlook with pessimistic analyst revisions has significantly damaged short-term market sentiment, leaving investors to grapple with near-term growth concerns.

Technical Analysis of Accenture PLC (ACN)

Technically, Accenture PLC (ACN) shows a MACD (12,26,9) value of -7.785, indicating a sell signal. The RSI at 20.855 suggests sell condition and the Williams %R at 96.713 suggests oversold condition. Please monitor closely.

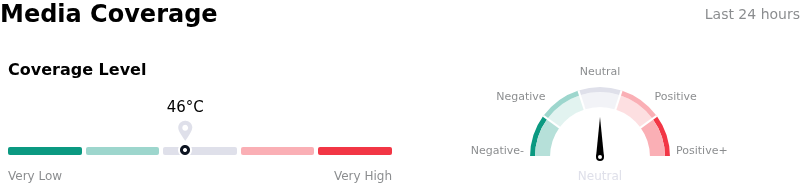

Media Coverage of Accenture PLC (ACN)

In terms of media coverage, Accenture PLC (ACN) shows a coverage score of 46, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Accenture PLC (ACN)

Accenture PLC (ACN) is in the Software & IT Services industry. Its latest annual revenue is $69.67B, ranking 6 in the industry. The net profit is $7.68B, ranking 14 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $0.00, a high of $0.00, and a low of $0.00.

More details about Accenture PLC (ACN)

Company Specific Risks:

- Guidance Downgrade and Q4 Forecast Miss: In its Q3 FY2026 earnings release on June 18, 2026, Accenture downgraded its full-year revenue growth guidance to 3%–4% in local currency (down from 3%–5%) and projected Q4 revenue of $17.75 billion to $18.40 billion, which falls short of Wall Street's consensus estimate of $18.47 billion.

- Geopolitical Headwinds and Middle East Disruptions: The ongoing conflict in West Asia has severely impacted high-margin discretionary consulting, causing a $100 million revenue deficit in Q3 and prompting a warning from CEO Julie Sweet of a cumulative $400 million hit to EMEA and Middle East operations in Q4 due to prolonged corporate decision-making.

- AI Cannibalization of Core Consulting Revenue: Following the earnings release, institutional analysts (including Morgan Stanley) expressed concerns that autonomous generative AI tools are actively cannibalizing traditional time-and-materials IT consulting demand, as enterprise clients choose to automate software development and workflow integrations internally instead of hiring external consultants.

- Slowing Bookings and U.S. Federal Spending Drag: Q3 new bookings fell 2% year-over-year to $19.32 billion, exacerbated by a 1% to 1.5% drag stemming from a spending slowdown in the U.S. Federal business. To combat this organic slowdown, Accenture announced a $4.175 billion cybersecurity acquisition of Dragos, runZero, and NetRise that is expected to be initially dilutive to earnings.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.