Accenture PLC Stock (ACN) Moved Down by 17.99% on Jun 18: What Investors Need To Know

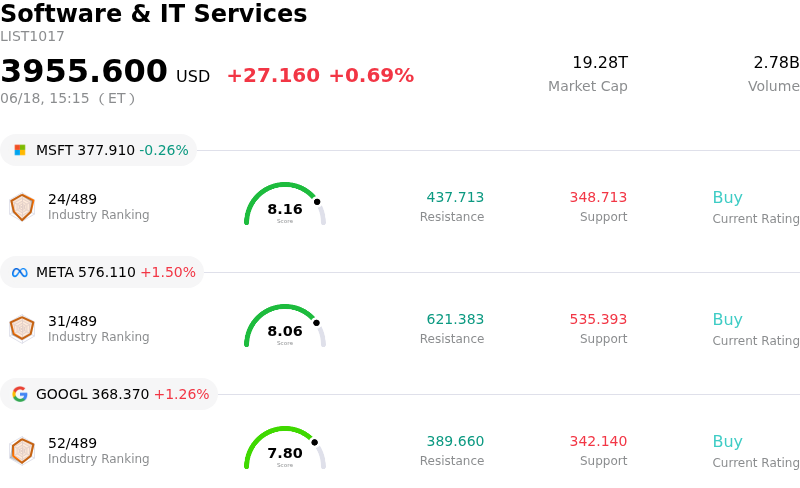

Accenture PLC (ACN) moved down by 17.99%. The Software & IT Services sector is up by 0.69%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) down 0.26%; Meta Platforms Inc (META) up 1.52%; Alphabet Inc Class A (GOOGL) up 1.26%.

What is driving Accenture PLC (ACN)’s stock price down today?

Accenture experienced a sharp decline in its share price following the release of its third-quarter fiscal 2026 financial results, which presented a mixed performance alongside revised full-year outlooks and massive strategic acquisitions. Although the company displayed operational resilience in several key areas, investors reacted negatively to cooling short-term demand signals and a substantial capital reallocation strategy.

The primary catalyst for the downward pressure was the combination of a revenue miss and slowing booking activity. Accenture reported quarterly revenue of $18.7 billion, representing a 6% year-over-year increase but falling short of Wall Street’s consensus estimate. While diluted earnings per share came in at $3.80, beating expectations, the top-line softness was compounded by a decline in new bookings. New bookings fell to $19.32 billion from $19.7 billion in the prior-year period, reflecting a broader pullback in discretionary consulting spend as enterprise clients remain cautious.

Investor sentiment was further dampened by the company’s revised business outlook. Management trimmed its expectations, forecasting full-year fiscal 2026 revenue growth of 3% to 4% in local currency. The lowered growth projections are partly due to a projected headwind from the company's U.S. federal business. This downward revision in revenue growth trajectory overshadowed the otherwise healthy expansion in operating margins to 17% and strong free cash flow generation of $3.6 billion.

In tandem with the earnings report, Accenture announced a massive strategic push into the cybersecurity sector, agreeing to acquire a majority stake in Dragos, along with full ownership of runZero and NetRise, for a combined enterprise value of approximately $4.18 billion. This transaction represents a core component of the company's expanded capital allocation plan, with full-year acquisition spending targets raised to $9 billion. While management positions these acquisitions as critical for securing long-term dominance in operational technology security, the market expressed immediate skepticism. Investors are highly sensitive to massive cash deployments during a period of decelerating organic growth, leading to concerns over near-term integration risks and diluted returns.

The combination of moderated revenue guidance, declining bookings, and aggressive capital expenditure on cybersecurity acquisitions has accelerated the stock's downward trend. With macro challenges persisting in the IT consulting landscape, institutional and retail investors are prioritizing immediate demand visibility over long-term strategic transformations, leading to a sharp reassessment of the company's valuation.

Technical Analysis of Accenture PLC (ACN)

Technically, Accenture PLC (ACN) shows a MACD (12,26,9) value of -3.745, indicating a sell signal. The RSI at 32.113 suggests neutral condition and the Williams %R at 99.762 suggests oversold condition. Please monitor closely.

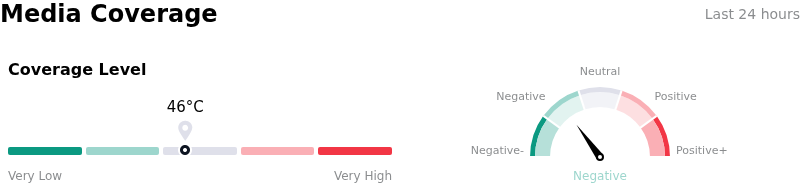

Media Coverage of Accenture PLC (ACN)

In terms of media coverage, Accenture PLC (ACN) shows a coverage score of 46, indicating a moderate level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Accenture PLC (ACN)

Accenture PLC (ACN) is in the Software & IT Services industry. Its latest annual revenue is $69.67B, ranking 6 in the industry. The net profit is $7.68B, ranking 14 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $235.49, a high of $329.00, and a low of $177.00.

More details about Accenture PLC (ACN)

Company Specific Risks:

- Narrowed FY2026 Guidance and Q4 Revenue Outlook Shortfall: In its Q3 FY2026 earnings release, Accenture trimmed its full-year local-currency revenue growth guidance to 3%–4% (down from 3%–5%) and projected Q4 revenues of $17.75B–$18.40B, trailing the Wall Street consensus of $18.48B due to delayed client decision-making. This triggered severe analyst target cuts and a sharp intraday stock drop of up to 19%.

- Severe Headwinds in U.S. Federal Government Segment: The company's U.S. federal business segment has emerged as a major growth drag due to slower procurement cycles and a wave of contract reviews, which management projects will shave 1% to 1.5% off the company’s overall fiscal 2026 growth rate.

- Balance Sheet Pressure from Debt-Funded M&A: Amid decelerating organic growth, Accenture announced plans to spend $4.18 billion to acquire operational technology security firms (Dragos, runZero, and NetRise) while simultaneously preparing to issue long-term debt, raising analyst concerns over capital allocation efficiency and complex integration risks.

- Geopolitical Friction and International Revenue Impact: Management disclosed that ongoing geopolitical conflicts, particularly in the Middle East, inflicted a direct $100 million negative impact on revenue during the quarter, with severe uncertainty surrounding the recovery timeline for enterprise client budgets in affected international markets.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.