Accenture PLC Stock (ACN) Moved Down by 4.13% on Jun 3: Key Drivers Unveiled

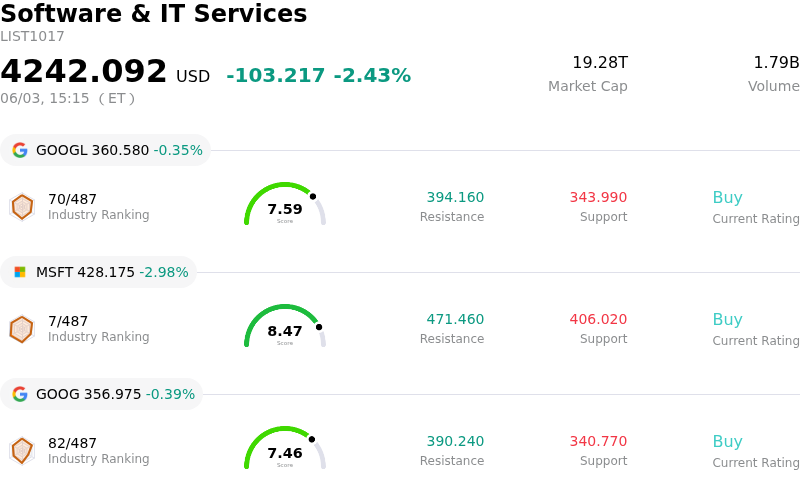

Accenture PLC (ACN) moved down by 4.13%. The Software & IT Services sector is down by 2.43%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Alphabet Inc Class A (GOOGL) down 0.39%; Microsoft Corp (MSFT) down 2.98%; Alphabet Inc Class C (GOOG) down 0.43%.

What is driving Accenture PLC (ACN)’s stock price down today?

Accenture's stock experienced significant downward movement due to a confluence of negative analyst sentiment and ongoing concerns impacting the IT services industry. A notable event contributing to this decline was Truist Securities' downgrade of Accenture's rating from "Buy" to "Hold" on June 1, 2026, accompanied by a substantial reduction in its price target. Citigroup also adjusted its price target downward, maintaining a neutral rating for the company.

The rationale behind these analyst adjustments points to several pressures. Analysts cited continued budget constraints among clients, leading to a shift in enterprise spending towards lower-margin cost-optimization projects. There are also growing concerns regarding increased competition from specialized Artificial Intelligence (AI) focused companies and the potential for AI technologies to disrupt or "cannibalize" Accenture's traditional core services and headcount-based pricing models. Geopolitical uncertainties have further weighed on client decision-making and demand trends, impacting Accenture's growth outlook.

Adding to the company-specific risks, Accenture faced headwinds from its U.S. federal business. In April 2026, federal agencies terminated a significant contract award for Military OneSource, which was held by Cognosante, a company acquired by Accenture. This contract was subsequently awarded to a different prime contractor, amplifying investor sensitivity around Accenture's federal exposure.

The upcoming third-quarter fiscal 2026 earnings report, expected on June 18, 2026, also likely contributed to investor caution. Anticipation and risk-reduction positioning ahead of these results frequently lead to volatility. Despite Accenture's proactive investments in AI capabilities through strategic acquisitions and partnerships, such as with AlphaSense announced on June 3, 2026, and a new joint venture with Mitsubishi Chemical, the prevailing concerns about industry dynamics and client spending appear to have outweighed these positive developments in the short term.

Technical Analysis of Accenture PLC (ACN)

Technically, Accenture PLC (ACN) shows a MACD (12,26,9) value of [-2.03], indicating a neutral signal. The RSI at 54.27 suggests neutral condition and the Williams %R at -27.92 suggests oversold condition. Please monitor closely.

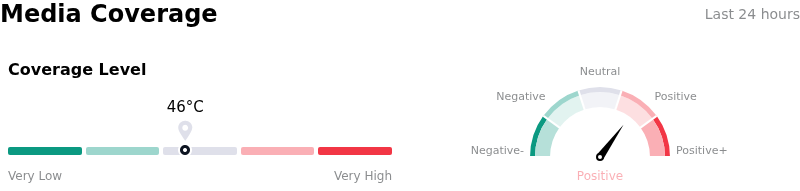

Media Coverage of Accenture PLC (ACN)

In terms of media coverage, Accenture PLC (ACN) shows a coverage score of 46, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Accenture PLC (ACN)

Accenture PLC (ACN) is in the Software & IT Services industry. Its latest annual revenue is $69.67B, ranking 6 in the industry. The net profit is $7.68B, ranking 14 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $249.26, a high of $329.00, and a low of $180.27.

More details about Accenture PLC (ACN)

Company Specific Risks:

- Truist Securities downgraded Accenture to a "Hold" rating on June 1, 2026, significantly reducing its price target, citing ongoing client budget pressures, heightened competition from AI pure-play companies, and potential AI-driven revenue cannibalization of traditional service models.

- The company faces increased risk of margin compression due to a shift in enterprise spending from higher-margin consulting projects towards lower-margin cost-optimization work, as noted by recent analyst commentary.

- Accenture's traditional headcount-based pricing models are vulnerable to disruption from evolving Artificial Intelligence capabilities, creating a risk of core revenue cannibalization and intensified competition.

- Ongoing investor sensitivity and concerns regarding Accenture's U.S. federal business exposure, including potential contract headwinds, are contributing to selling pressure.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.