ServiceNow Inc Stock (NOW) Moved Down by 6.26% on Jun 3: Drivers Behind the Movement

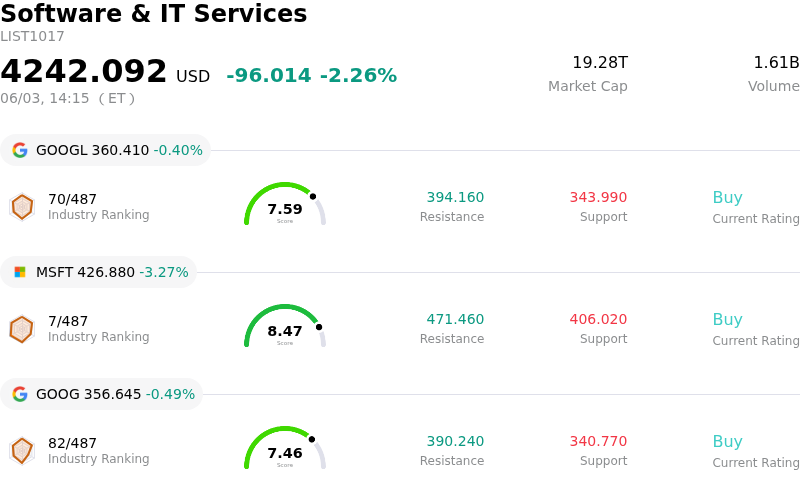

ServiceNow Inc (NOW) moved down by 6.26%. The Software & IT Services sector is down by 2.26%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Alphabet Inc Class A (GOOGL) down 0.40%; Microsoft Corp (MSFT) down 3.27%; Alphabet Inc Class C (GOOG) down 0.49%.

What is driving ServiceNow Inc (NOW)’s stock price down today?

The current price movement for ServiceNow (NOW) appears to be primarily driven by a combination of market-wide pressures and recent company-specific sentiment shifts. The stock had experienced a robust rally leading up to this point, fueled by strong first-quarter 2026 financial performance, which exceeded revenue estimates and led to increased full-year subscription revenue guidance. This upward momentum left the stock vulnerable to a technical correction and profit-taking by investors, a common occurrence after substantial gains.

Adding to this, the broader market experienced a downturn today, significantly impacting equities, particularly within the technology sector. Heightened geopolitical tensions between the US and Iran have led to a rise in crude oil prices, contributing to inflation concerns and increasing the likelihood of further interest rate adjustments by the Federal Reserve. This macroeconomic environment has prompted investors to move away from growth-oriented assets, contributing to a sector-wide decline that has affected software companies.

Furthermore, recent analyst sentiment has introduced some caution. Yesterday, a new "Sell" rating for ServiceNow was issued, citing concerns over gross margins and the potential for deal delays, which likely carried over into today's trading. While the company's aggressive strategy in integrating artificial intelligence into its platform and recent strategic partnerships have been well-received by many, reports indicating a year-over-year decline in gross margins and anticipated compression due to cloud costs and acquisition integration have weighed on investor perception. The acquisition of Armis, while expanding market reach, is expected to create near-term headwinds for operating and free cash flow margins.

Despite these immediate headwinds, ServiceNow continues to demonstrate strong underlying fundamentals, including a focus on AI-driven growth and a high customer retention rate. However, for today's trading, the confluence of profit-taking, broader market weakness, and specific concerns regarding margins and competitive dynamics appear to be the dominant factors influencing the share price movement.

Technical Analysis of ServiceNow Inc (NOW)

Technically, ServiceNow Inc (NOW) shows a MACD (12,26,9) value of [3.19], indicating a buy signal. The RSI at 68.70 suggests neutral condition and the Williams %R at -21.48 suggests oversold condition. Please monitor closely.

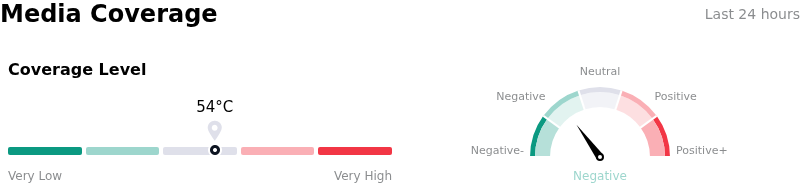

Media Coverage of ServiceNow Inc (NOW)

In terms of media coverage, ServiceNow Inc (NOW) shows a coverage score of 54, indicating a moderate level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of ServiceNow Inc (NOW)

ServiceNow Inc (NOW) is in the Software & IT Services industry. Its latest annual revenue is $13.28B, ranking 28 in the industry. The net profit is $1.75B, ranking 30 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $143.92, a high of $236.00, and a low of $85.00.

More details about ServiceNow Inc (NOW)

Company Specific Risks:

- UBS downgraded ServiceNow, citing weakening confidence in the company's AI competitive positioning and increasing budget pressure on non-AI application software, leading to expectations of smaller earnings beats and limited upside to guidance.

- UBS lowered the estimated current remaining performance obligation (RPO) growth for 2026 from 20% to 16%, indicating a deceleration in future subscription revenue expansion.

- ServiceNow anticipates lower full-year subscription adjusted gross margins due to integration costs from recent acquisitions and faces headwinds to subscription revenue growth from delayed large on-premise deals in the Middle East caused by geopolitical conflicts.

- The company faces intensified competitive pressure from other major tech players and AI-native startups, as enterprise spending shifts towards AI solutions, potentially leading to pricing pressure and longer sales cycles.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.