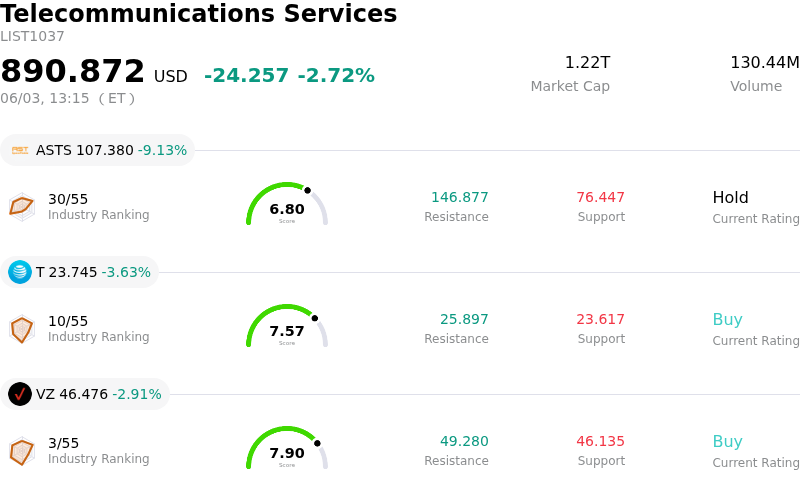

AT&T Inc Stock (T) Moved Down by 3.63% on Jun 3: A Full Analysis

AT&T Inc (T) moved down by 3.63%. The Telecommunications Services sector is down by 2.72%. The company underperformed the industry. Top 3 stocks by turnover in the sector: AST SpaceMobile Inc (ASTS) down 9.13%; AT&T Inc (T) down 3.63%; Verizon Communications Inc (VZ) down 2.91%.

What is driving AT&T Inc (T)’s stock price down today?

AT&T's stock experienced notable downward movement today, primarily influenced by an analyst downgrade and prevailing concerns regarding intensifying competition and its financial positioning. Oppenheimer lowered its rating on AT&T from "Outperform" to "Perform," citing potential risks stemming from the emergence of low-earth-orbit satellite constellations. The analyst noted that these new satellite services could attract a significant number of subscribers away from traditional wireless carriers, predicting an annual shift of over 2 million subscribers and potentially capturing a substantial market share by 2030.

This revised outlook suggests that AT&T's average revenue per user may face increased pressure, exacerbated by existing robust competition from other major telecommunication providers. The company also anticipates significant capital expenditure for an upcoming AWS-3 auction, which could further strain its financial resources. Concerns about the company's financial health were also highlighted by a low Altman Z-score, which indicates potential financial distress or bankruptcy risk within the next two years.

While AT&T had recently reiterated its 2026 and multi-year financial guidance, including expectations for improved adjusted EBITDA and EPS growth, and higher free cash flow through 2028, the market appears to be reacting more strongly to the immediate competitive threats and the analyst's more cautious stance. The broader telecommunications industry is currently navigating challenges related to network monetization and substantial infrastructure investments, which contribute to a complex operating environment for companies like AT&T.

Other recent company announcements, such as streamlining fiber internet plans and introducing bundle discounts, or a new administrative fee for prepaid customers, did not seem to offset the negative sentiment generated by the analyst downgrade and the underlying competitive and financial concerns it highlighted. While some analysts still maintain a "Buy" consensus rating on the stock with a median price target suggesting upside, the impact of Oppenheimer's more conservative assessment appears to have been a significant driver of today's stock performance.

Technical Analysis of AT&T Inc (T)

Technically, AT&T Inc (T) shows a MACD (12,26,9) value of [-0.42], indicating a neutral signal. The RSI at 40.17 suggests neutral condition and the Williams %R at -53.53 suggests oversold condition. Please monitor closely.

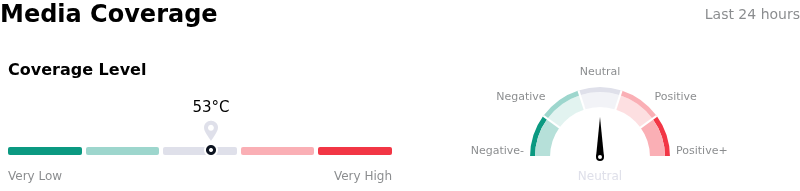

Media Coverage of AT&T Inc (T)

In terms of media coverage, AT&T Inc (T) shows a coverage score of 53, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of AT&T Inc (T)

AT&T Inc (T) is in the Telecommunications Services industry. Its latest annual revenue is $125.65B, ranking 2 in the industry. The net profit is $21.89B, ranking 1 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $29.85, a high of $36.00, and a low of $25.00.

More details about AT&T Inc (T)

Company Specific Risks:

- Oppenheimer downgraded AT&T to "Perform" from "Outperform" on June 3, 2026, citing rising competitive threats from Low Earth Orbit (LEO) satellite constellations that are expected to challenge long-term broadband subscriber growth and mobile services.

- AT&T demonstrates weak financial strength with a low score of 4/10 and an Altman Z-score of 0.96, indicating potential financial distress and bankruptcy risk within the next two years.

- Analysts express concerns that AT&T's fiber penetration may disappoint, potentially stopping at 50 million homes instead of the projected 60 million by 2030, raising questions about the feasibility of its growth projections in this critical area.

- The company faces potential pressure on its average revenue per user (ARPU) due to heightened competition from major telecommunications peers and the significant capital expenditure requirements for the upcoming AWS-3 auction.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.