Salesforce Inc Stock (CRM) Moved Down by 5.73% on Jun 2: Drivers Behind the Movement

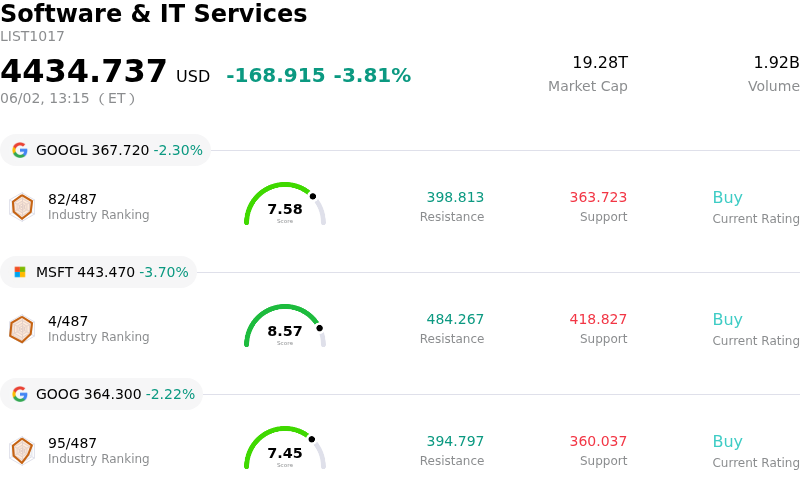

Salesforce Inc (CRM) moved down by 5.73%. The Software & IT Services sector is down by 3.81%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Alphabet Inc Class A (GOOGL) down 2.30%; Microsoft Corp (MSFT) down 3.70%; Alphabet Inc Class C (GOOG) down 2.22%.

What is driving Salesforce Inc (CRM)’s stock price down today?

Salesforce (CRM) experienced a notable decline in share price today, which appears to be a reaction to a combination of factors following its recent earnings report. Despite reporting strong first-quarter fiscal 2027 results that surpassed analyst expectations for both revenue and adjusted earnings per share, the company's forward guidance for the second quarter and full fiscal year 2027 fell slightly below consensus estimates. This softer outlook has fueled investor anxiety, particularly concerning the potential impact of AI agents on traditional software demand and ongoing weaknesses in the marketing and commerce segments, as well as a slowdown in Tableau bookings.

The decline can also be attributed to profit-taking after the stock saw a significant rally in the previous trading session, which was driven by the impressive first-quarter results, a substantial share repurchase program, and an increased quarterly dividend. Several analyst firms have also adjusted their price targets on Salesforce in the days surrounding the earnings report, with some trimming their targets or maintaining more cautious ratings like "Underperform" or "Neutral," citing concerns about AI monetization pathways and the pace of AI adoption translating into revenue growth. This suggests a divergence in narrative among analysts regarding the company's ability to capitalize on its AI investments and maintain its growth trajectory amidst increasing competition.

Furthermore, there have been recent discussions and reports about Salesforce's potential exposure to data breaches due to misconfigurations in its Experience Cloud, and a past Salesforce Aura data breach investigation, which could contribute to negative market sentiment. The broader market is not providing strong upward momentum, indicating that today's movement is primarily driven by company-specific dynamics rather than macroeconomic trends. The stock is also grappling with technical headwinds, remaining below its 200-day moving average and showing bearish moving-average crossover patterns, suggesting that the longer-term downtrend has not been fully reversed.

Technical Analysis of Salesforce Inc (CRM)

Technically, Salesforce Inc (CRM) shows a MACD (12,26,9) value of [-0.54], indicating a neutral signal. The RSI at 70.60 suggests buy condition and the Williams %R at -3.70 suggests oversold condition. Please monitor closely.

Media Coverage of Salesforce Inc (CRM)

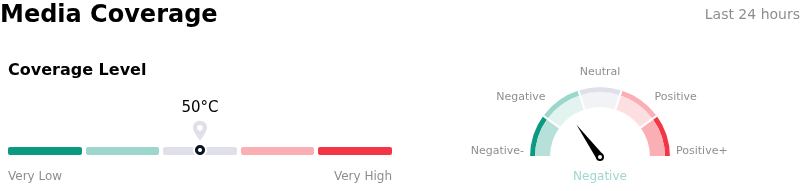

In terms of media coverage, Salesforce Inc (CRM) shows a coverage score of 50, indicating a moderate level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Salesforce Inc (CRM)

Salesforce Inc (CRM) is in the Software & IT Services industry. Its latest annual revenue is $41.52B, ranking 13 in the industry. The net profit is $7.46B, ranking 15 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $254.40, a high of $475.00, and a low of $160.00.

More details about Salesforce Inc (CRM)

Company Specific Risks:

- Salesforce provided a softer-than-expected Q2 revenue outlook and full-year fiscal year 2027 revenue guidance that marginally missed some analyst expectations, indicating potential near-term growth deceleration despite a strong Q1 performance.

- Core Sales and Service Cloud products are experiencing structural growth deceleration, with growth rates around 7% in constant currency, half of the previous year, influenced by slower seat expansion among large enterprises and extended customer renewal cycles.

- Analyst skepticism persists regarding the effective monetization of new AI innovations (e.g., Agentforce) and the transition away from the traditional seat-based licensing model, with Bank of America reiterating an "Underperform" rating and a $160 price target.

- The recent $8 billion Informatica acquisition is anticipated to introduce greater license revenue volatility and presents integration complexities, with accretion not expected until fiscal year 2027.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.