TradingKey Wall Street Weekly Report: Geopolitical Risks Push up Oil Prices; US Stocks Rise Narrowly, Focusing on AI and Defense Sectors

AI Podcast

The week of May 18-24, 2026, saw U.S. equity markets advance, led by energy and tech sectors, with the S&P 500 nearing its eighth consecutive weekly gain. Geopolitical tensions, particularly the U.S.-Iran conflict, fueled inflation concerns and oil price hikes. Federal Reserve officials expressed hawkish sentiment regarding potential rate hikes, coinciding with the appointment of Kevin Warsh as new Chairman. Consumer sentiment hit an all-time low. Nvidia reported strong earnings, though revenue excluded China due to restrictions. Investors rotated towards mega-cap tech and defensible names. Key risks include persistent inflation and geopolitical instability.

Previous Week’s Market Review & Analysis

Macroeconomic Landscape:

The macroeconomic landscape for the week of May 18-24, 2026, was primarily influenced by persistent geopolitical tensions and evolving monetary policy signals. The ongoing U.S.-Iran conflict and its impact on the Strait of Hormuz continued to constrain global oil supply, keeping Brent crude near multi-year highs and sustaining inflation concerns. Federal Reserve officials expressed intensifying concerns about inflation stemming from the Iran war, with a growing number considering laying the groundwork for a possible rate hike. Kevin Warsh was named the new Federal Reserve Chairman, succeeding Jerome Powell, and is scheduled to be sworn in at the end of this week. Key economic data released included PMI data for Manufacturing and Services sectors, ISM Services New Orders, and ISM Services Prices. Housing Starts, Building Permits, and Weekly Jobless Claims were reported. The University of Michigan's preliminary consumer sentiment for May reached an all-time low.

Market Performance Overview:

U.S. equity markets posted positive gains for the week, with the S&P 500 on track for its eighth consecutive weekly advance. The S&P 500 index was up approximately 1%, the Nasdaq Composite gained 0.7%, and the Russell 2000 increased by 2.7% for the week. Energy was the standout sector, surging 7.03%, while Information Technology also gained 1.21%. Consumer Discretionary was the worst performer, falling 3.04%. The equal-weighted S&P 500 fell 1.29%, and small-cap benchmarks declined sharply, indicating a rotation towards larger, more defensible names.

Key Events Analysis:

The Federal Open Market Committee (FOMC) Minutes from the April 28-29 meeting were released on Wednesday, May 20, revealing a divided committee with increasing hawkish sentiment regarding inflation and potential rate hikes. Several Federal Reserve officials, including Governor Michael S. Barr and Governor Christopher J. Waller, delivered speeches. Corporate earnings continued with notable reports. Nvidia announced "solid beat and raise" quarterly results on Wednesday, May 20, posting record revenue of $81.6 billion and projecting $91 billion for the next quarter, notably excluding China Data Center revenue due to geopolitical restrictions. Other companies reporting included Palo Alto Networks, Home Depot, Keysight Technologies, Analog Devices, Intuit, Lowe's Companies, Medtronic, Target, and TJX Companies. A U.S.-China leaders' summit concluded with investor disappointment over the lack of major agreements on the Middle East conflict.

Flows & Sentiment:

Market sentiment remained sensitive to geopolitical developments, particularly surrounding the U.S.-Iran conflict and oil prices. The University of Michigan's preliminary consumer sentiment for May recorded an all-time low. Investors rotated towards larger, more defensible equity names, moving away from small-cap and equal-weight strategies. Market volatility was observed as extremely high, with significant gap risks at week openings.

Overall Assessment:

The market's logic for the week was primarily driven by geopolitical tensions in the Middle East and their persistent impact on oil prices and inflation expectations, often overshadowing traditional economic indicators. Despite a resilient performance in major indices, the market exhibited a narrow rally, heavily concentrated in mega-cap technology and AI-related stocks. The current phase of market behavior is characterized by a "wait-and-see" approach regarding geopolitical outcomes, leading to unpredictable price movements.

Next Week’S Key Market Drivers and Investment Outlook

Upcoming Events:

The U.S. markets will be closed on Monday, May 25, for Memorial Day. Key economic data releases scheduled for next week include the Consumer Confidence report for May on Tuesday, May 26. On Thursday, May 28, the U.S. core PCE price index for April and the second estimate of U.S. Gross Domestic Product for the first quarter of 2026 will be released.

Market Logic Projection:

Macro conditions will likely continue to be dominated by geopolitical risks, particularly the U.S.-Iran conflict and its potential influence on energy prices and global supply chains. The upcoming core PCE data will be crucial in shaping inflation expectations and influencing the Federal Reserve's policy trajectory under the new Chair, Kevin Warsh, whose first FOMC meeting is anticipated in June. Micro-fundamental factors will include ongoing corporate earnings announcements from technology and retail sectors, with continued optimism surrounding AI investments.

Strategy & Allocation Recommendations:

Investors are advised to prioritize robust risk management strategies due to the heightened geopolitical uncertainty and market volatility. Maintaining a balanced portfolio is crucial, especially given the S&P 500's record highs and the concentrated nature of recent gains in mega-cap technology. Strategic allocation should include continued exposure to AI-driven technology, coupled with diversification across other sectors and close monitoring of broader economic fundamentals.

Risk Alerts:

Key risks include the potential for persistent inflation, especially if energy prices continue their upward trend due to unresolved geopolitical tensions in the Middle East. Elevated borrowing costs and stubborn inflation could negatively impact corporate earnings. Deteriorating consumer confidence and rising gasoline prices pose a risk of consumer spending weakness, potentially shifting discretionary spending. The market remains highly sensitive to any developments or news related to the Persian Gulf.

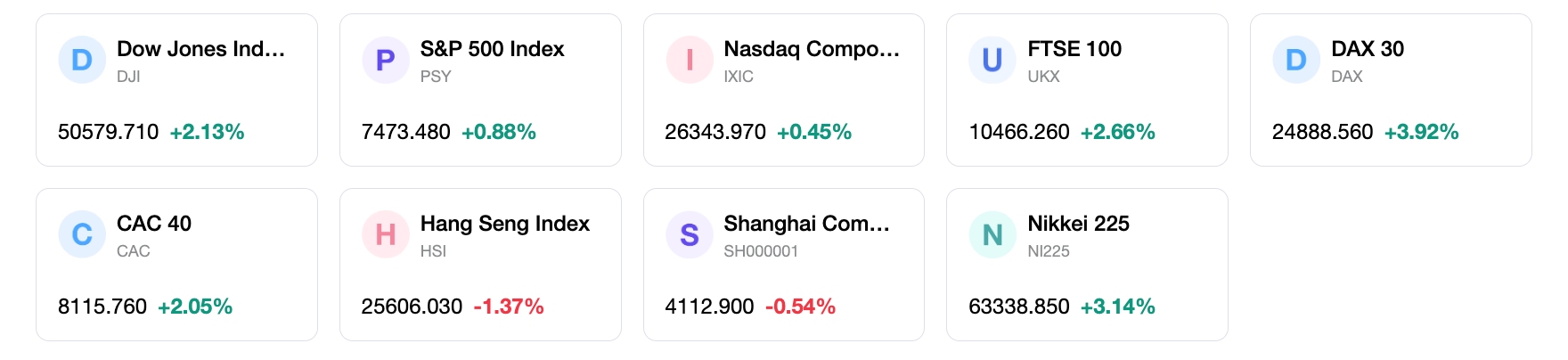

Markets Weekly

5-day index performance

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.