Warren Buffett Keeps Dumping Apple Shares: Here's the Stock He Is Buying Instead

Another quarter, another Apple (NASDAQ: AAPL) sale from Warren Buffett. The legendary investor sold a massive chunk of Apple stock yet again in the third quarter, estimated to be worth more than $20 billion, or 100 million shares. Berkshire Hathaway -- the company Buffett controls -- still owns $70 billion of Apple stock, but it is now a much smaller position than at the start of the year.

Why is Buffett selling? This article will get into the likely culprit a little later. More importantly, what is Buffett buying today? Not much, but Berkshire Hathaway did take a stab and acquired 3.5% of Domino's Pizza (NYSE: DPZ) last quarter. Here's why the company may look attractive to Buffett and his investment team at the moment.

Why Berkshire Hathaway keeps trimming Apple

The Apple investment has generated over $100 billion in capital gains for Berkshire Hathaway. Throughout 2024, Buffett has begun to realize a lot of these gains, raising Berkshire Hathaway's cash position to more than $300 billion.

He is likely shying away from Apple as such a large position in the Berkshire Hathaway portfolio for a simple reason: valuation. It has nothing to do with market timing, or Buffett making a bet that the stock market is going to crash anytime soon. The stock just looks overvalued at these prices.

And it is hard to disagree with this sentiment. At current prices, Apple is trading at a price-to-earnings ratio (P/E) of 37. While not an egregious earnings ratio for a high-growth stock, Apple isn't a fast grower anymore. In fact, it is barely growing at all, and at a significantly slower pace than inflation.

In the last three years, Apple's revenue is only up 3% on a cumulative basis. Buffett is likely concerned about the stock underperforming due to this tepid growth combined with a high earnings ratio. It is not like Apple is now a bad business; just one where the stock is priced to perfection. It is hard to compound your capital owning something like this.

Domino's Pizza: The next restaurant franchising giant?

On the other side of the spectrum, Berkshire Hathaway initiated a new position in Domino's Pizza last quarter, now owning a sizable chunk of the business. This is not nearly as large of a position as Apple, but it is curious that Berkshire Hathaway is buying the stock now.

Buffett famously likes the capital-light franchising model for restaurants, and has been an ardent fan of McDonald's business success (along with its food) for a long time. Domino's Pizza runs a similar franchising model for its pizza shops.

Like McDonald's a few decades ago, Domino's is now planning a major global expansion for its franchise. It is planning to open 800 to 850 new stores this year. Store count at the end of last quarter was 21,000. If it adds around 1,000 stores a year, the company will reach the same store level count as McDonald's today (over 40,000) in around 20 years. This lines up with management's long-term guidance of 7% sales growth and 8% operating income growth from 2026 to 2028.

Berkshire Hathaway is likely attracted to Domino's because of this long-term growth potential. As he likes to say, growth and value are tied at the hip. If a company is set to grow its earnings at a durable rate for a long while, you can pay more for its current earnings and still make money. This is unlike Apple, which trades at a high P/E, but with low growth.

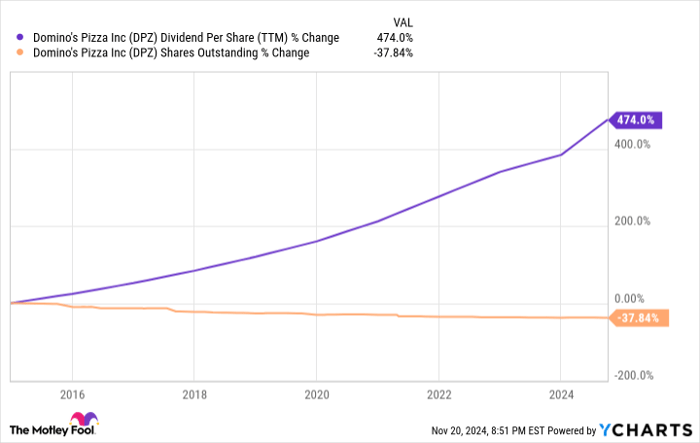

DPZ Dividend Per Share (TTM) data by YCharts

Should you buy Domino's stock?

Even with a better growth profile than Apple -- or really, the average stock in the market -- Domino's trades at a P/E ratio of 26, which is below the S&P 500 (SNPINDEX: ^GSPC) average of 30. It may be simplifying things, but this contradiction should make Domino's Pizza stock a buy at current prices.

Don't forget that the company's robust capital returns program too. Domino's has grown its dividend per share by 474% in the last 10 years, while bringing its shares outstanding down by 38% due to a consistent share repurchase program. There's no reason to think both trends won't continue for the foreseeable future, either.

Add these into the mix, and Domino's Pizza looks like a foolproof stock to buy and hold for the long term. No wonder Buffett and Berkshire Hathaway are buying.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $368,053!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,533!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $484,170!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 18, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Berkshire Hathaway, and Domino's Pizza. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.