Prediction: This Buzzworthy Stock-Split Stock Will Plunge by 50% (if Not More) Over the Next 12 Months

Though it's been a bit bumpy at times, the bulls have been in the driver's seat on Wall Street for the last two years. Recently, we've witnessed the iconic Dow Jones Industrial Average, widely followed S&P 500, and innovation-inspired Nasdaq Composite, all reach record-closing highs.

Although better-than-expected corporate earnings and hype surrounding the artificial intelligence (AI) revolution have each played key roles in lifting the broader market higher, no discussion of bull market catalysts in 2024 would be complete without mentioning stock-split euphoria.

Image source: Getty Images.

A stock split allows publicly traded companies the opportunity to adjust their share price and outstanding share count by the same factor. Despite these potential changes, splits are superficial in the sense that they don't alter a company's market cap or in any way affect its operating performance.

Since consumer goods colossus Walmart kicked things off with a 3-for-1 stock split in late February, more than a dozen prominent/market-leading businesses have followed suit and completed splits of their own. All but one of these splits has been of the forward variety, which are designed to make shares more nominally affordable for everyday investors and/or employees who may not have access to fractional-share purchases.

Since 1980, companies that have announced forward splits have vastly outperformed the benchmark S&P 500. Based on returns in the 12 months following a split announcement, the stock-split stocks have gained 25.4% versus 11.9% for the S&P 500 over the same span, according to Bank of America Global Research.

But this doesn't mean all stock-split stocks are universally worth buying. While some stand out for all the right reasons, one has all the hallmarks of a disaster waiting to happen.

Wall Street's buzziest stock-split stock has more-than-quadrupled in 2024

Though I've been decidedly critical of highfliers like Nvidia and Chipotle Mexican Grill, there's another stock-split stock whose valuation is far more egregious. I'm talking about AI enterprise analytics software provider MicroStrategy (NASDAQ: MSTR).

Shares of MicroStrategy have catapulted higher by more than 300% on a year-to-date basis, as well as 1,710% since this decade began. Its rapid ascent encouraged its board to announce a 10-for-1 forward split in July, which went into effect following the close of trading on August 7.

Although MicroStrategy's core business has, for decades, been enterprise analytics software, and it's attempted to ride the AI wave with this operating segment, the company's nearly $52 billion market cap has little to with AI or software. Rather, Bitcoin (CRYPTO: BTC) is now the wind in MicroStrategy's sails.

Bitcoin is the largest digital currency by market value and is viewed as the pioneer among cryptocurrencies. It's enjoyed first-mover advantages for more than a decade, and is highly sought after by crypto investors for its perceived scarcity -- only 21 million Bitcoin will ever be mined.

MicroStrategy is the largest corporate holder of Bitcoin. Based on an 8-K filing from the company with the Securities and Exchange Commission on Sept. 20, it held 252,220 Bitcoin at an average cost of $39,266 per token. On an all-in basis, including fees and expenses, MicroStrategy has spent $9.9 billion to acquire 1.2% of an eventual 21 million Bitcoin.

As of this writing in the late evening hours of Oct. 29, a single Bitcoin will set investors back $72,481, which is close to its all-time intra-day high. It also means MicroStrategy's Bitcoin portfolio has increased in value by 85% from its cost basis. In other words, there are tangible reasons why the company's shareholders are excited.

But widen the lens a bit and you'll find plenty of reason to believe MicroStrategy's stock will plunge 50%, or significantly more, over the next 12 months.

Image source: Getty Images.

MicroStrategy is the mother of all cryptocurrency stock bubbles

There isn't just one reason I can point to that explains why MicroStrategy's stock could plummet over the next year. Rather, it's a confluence of factors that suggest it's the mother of all bubbles among cryptocurrency stocks.

The most front-and-center of all issues with MicroStrategy is the unjustified premium for its Bitcoin assets. Based on the aforementioned $72,481 current price for a single Bitcoin, MicroStrategy's 252,220 tokens are worth $18.28 billion. But it ended the Oct. 29 trading session with a market cap of $51.7 billion. Conservatively, the company's enterprise analytics software operations are worth $1 billion. This means a value of $50.7 billion is currently being assigned to MicroStrategy's Bitcoin portfolio, which is worth $18.28 billion.

Let me put this valuation gap in a different context. If you're a Bitcoin optimist and believe it'll head higher, you can purchase tokens right now for $72,481, not including nominal commission fees. Comparatively, if you're buying shares of MicroStrategy, you're paying a 177.35% premium to the current price for Bitcoin, or roughly $201,000 per token. There's absolutely no reason for this milewide disparity to exist.

To make matters worse, MicroStrategy has been funding its aggressive Bitcoin purchases via convertible-debt offerings. Following its latest upsized offering, the company has $4.274 billion in aggregate indebtedness and estimated annual interest expenses of $34.6 million.

Admittedly, the interest expense is exceptionally low, which is a function of having a fairly liquid asset (Bitcoin) that MicroStrategy could sell, if need be. Nevertheless, the company's only revenue-generating segment is its AI enterprise analytics software division. Through the first-half of 2024, MicroStrategy generated only $5.26 million in net cash from its operating activities. In other words, the company doesn't have sufficient cash flow to service its outstanding debt.

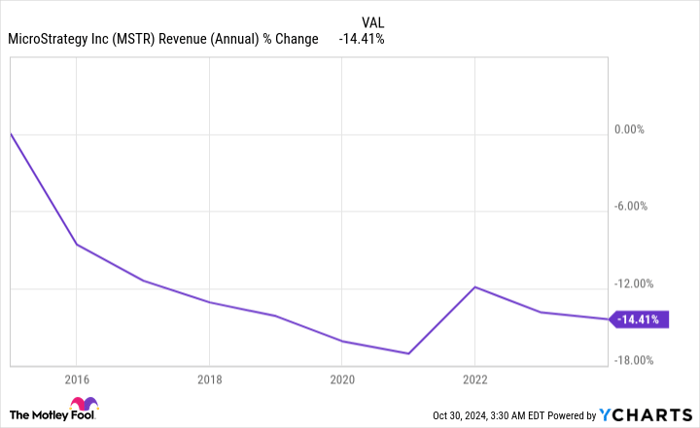

MSTR Revenue (Annual) data by YCharts.

Something else I'll add to the above is that the growth engine for MicroStrategy's software division stalled a long time ago. The company's annual sales have dipped by 14.4% over the trailing decade, which leaves little hope of a rebound that would cover the company's estimated annual interest expenses.

The nail in the coffin for MicroStrategy is that Bitcoin's first-mover advantages have, arguably, gone by the wayside. Multiple blockchain networks offer faster and cheaper settlement than Bitcoin. Meanwhile, its perceived scarcity is a function of lines of computer code that can be changed with community consensus.

MicroStrategy has all the hallmarks of being in a mammoth bubble, which makes it a stock-split stock that's set to plunge.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,492!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,204!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $409,559!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 28, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Sean Williams has positions in Bank of America. The Motley Fool has positions in and recommends Bank of America, Bitcoin, Chipotle Mexican Grill, Nvidia, and Walmart. The Motley Fool recommends the following options: short December 2024 $54 puts on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.