This Dow Jones Dividend Stock Is Packed With Potential, but Is It a Buy Now?

Honeywell International (NASDAQ: HON) fell a little over 5% on Oct. 24 despite reporting better-than-expected third-quarter earnings. The industrial conglomerate updated its full-year targets and gave investors insight into its strategic plans to get the company back on track toward more meaningful growth.

In September, the Dow Jones Industrial Average component raised its dividend for the 14th consecutive year to $4.52 per share -- representing a forward yield of 2.2%. Here's what you need to know from Honeywell's latest report and if the dividend stock is worth buying now.

Image source: Getty Images.

From Wall Street darling to laggard

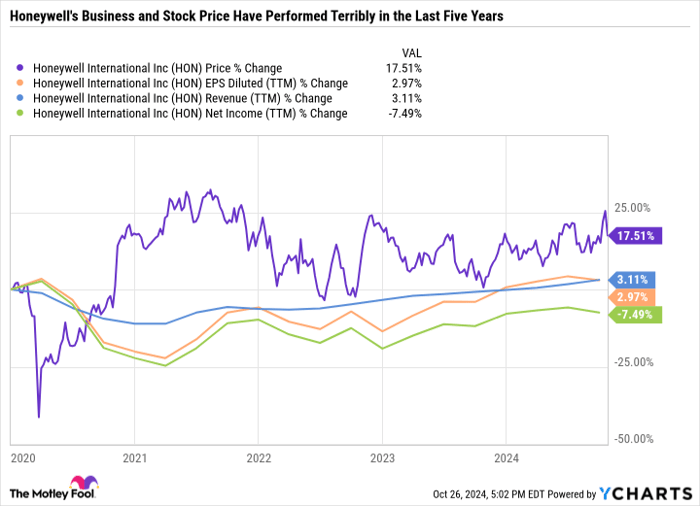

Honeywell's stock price soared 374% during the 2010s -- crushing the 190% gain in the S&P 500. But the stock price has languished for the last four years, heavily underperforming the market.

Honeywell's performance, especially in its aerospace segment, nosedived during the COVID-19 pandemic -- which was understandable given the commercial airline industry ground to a halt. Investors were willing to give Honeywell a pass so long as it returned to growth during the post-pandemic recovery. But Honeywell's results have continued to disappoint.

The conglomerate serves various business-to-business customers in manufacturing, energy, logistics and warehouses, healthcare, and more. When the business is right, Honeywell is a highly diversified cash cow that can offset the cyclical nature of some of these end markets by offering a broad range of products and services.

But Honeywell has failed to return to its pre-pandemic form, blaming weak demand, supply chain challenges, inflation, and macroeconomic factors. As you can see in the chart, Honeywell's stock price is up just 17.5% in the last five years, which is fair considering revenue and earnings per share (EPS) have gone practically nowhere. EPS is only up due to buybacks, as net income has fallen during this period.

Honeywell's turnaround strategy

There are many reasons for Honeywell's lackluster performance. But the simplest is that it became big, bulky, and bogged down by a lack of flexibility and innovation. Honeywell recognized that change was in order, and it made an aggressive plan to make a flurry of acquisitions and divest and simplify its business to align with its three highest-conviction megatrends: automation, the future of aviation, and the energy transition.

So far in 2024, Honeywell has spent over $9 billion on mergers and acquisitions (M&A) and a total of around $14 billion on capital expenditures, dividends, and share repurchases, putting it on track to spend at least $25 billion on these efforts through 2025.

The improvements are a step in the right direction, but Honeywell is still far from returning to its pre-pandemic growth rate. In the recent quarter, Honeywell grew organic sales by just 3% and expects full-year organic growth of 3% to 4%. Throw in some cost reductions and buybacks, and the company expects adjusted EPS growth of 7% to 8%. That's a decent level, but certainly not enough to justify a higher valuation.

Honeywell sports a price-to-earnings (P/E) ratio of just 24, which isn't dirt cheap but it is slightly below the company's five-year median P/E. But the run-up in the broader market has pushed the valuations of other blue chip dividend stocks above historic levels. Honeywell must prove its investments are worth it before it can justify a higher valuation.

Levering up

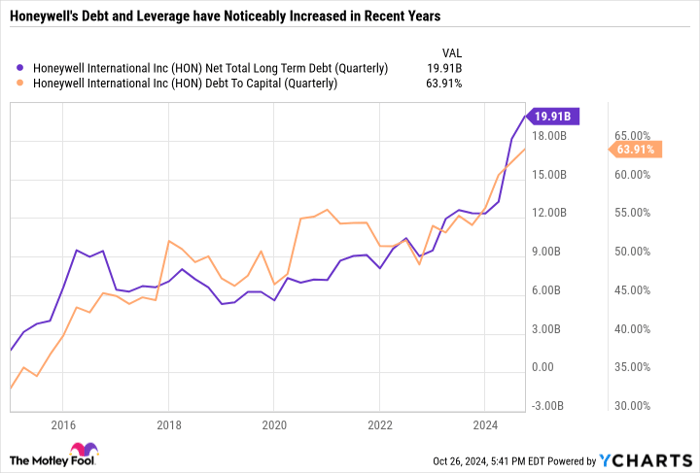

Honeywell's investments have come at a high price. In recent years, it has taken on a lot of debt, which has increased its leverage.

HON Net Total Long Term Debt (Quarterly) data by YCharts

Honeywell's balance sheet was in impeccable shape, and its leverage was low, so it had room to take on debt. Leverage is a double-edged sword, as it can accelerate growth and amplify a bad decision's impact. The state of Honeywell's balance sheet puts pressure on the company to prove to investors that it is allocating capital responsibly.

Honeywell has work to do

Honeywell's investment thesis is fairly straightforward. Investors who agree with the megatrends Honeywell is targeting and the way it is reshaping its portfolio to capitalize on those trends may want to consider buying the stock.

Folks who believe Honeywell should look inward and focus on organic growth rather than doing a lot of M&A and levering up its balance sheet may want to pass on Honeywell.

Honeywell has a decently attractive valuation and an OK dividend yield. But nothing about the company makes it a screaming buy at this time.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,492!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,204!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $409,559!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 28, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.