Accenture PLC Stock (ACN) Moved Down by 7.28% on Jun 22: Key Drivers Unveiled

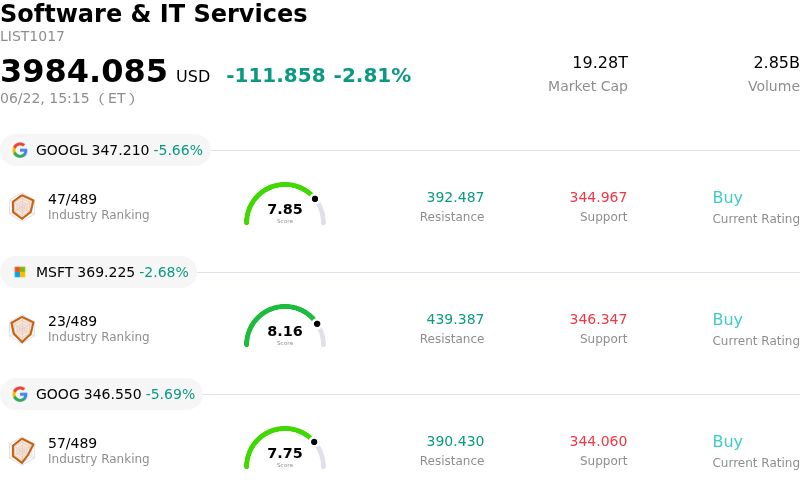

Accenture PLC (ACN) moved down by 7.28%. The Software & IT Services sector is down by 2.81%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Alphabet Inc Class A (GOOGL) down 5.66%; Microsoft Corp (MSFT) down 2.66%; Alphabet Inc Class C (GOOG) down 5.69%.

What is driving Accenture PLC (ACN)’s stock price down today?

Accenture's stock experienced significant downward pressure, continuing a volatile trend following its recent third-quarter fiscal 2026 earnings release. While the professional services giant surpassed Wall Street's bottom-line estimates and expanded its operating margins, several underlying challenges in the report triggered a wave of cautious analyst revisions and sent shares lower.

The primary catalyst for the decline is a combination of weak new bookings and trimmed full-year guidance. New bookings for the quarter fell year-over-year, indicating a slowdown in pipeline conversion. Consequently, management lowered the top end of its full-year fiscal 2026 revenue growth forecast. The company attributed this deceleration to three macro headwinds: a negative impact from geopolitical conflicts in the Middle East, clients deferring large managed-service agreements into the next fiscal year due to a wait-and-see attitude toward the Federal Reserve’s higher-for-longer interest rate environment, and persistent weakness in U.S. federal consulting sales.

Further impacting investor sentiment was Accenture’s concurrent announcement of a massive cybersecurity acquisition. The company agreed to invest billions of dollars to acquire a majority stake in Dragos and full ownership of runZero and NetRise. Although this strategic move significantly expands Accenture’s foothold in the rapidly growing operational technology security sector, the massive cash outlay is expected to be dilutive to earnings in the short term, introducing integration risks and adding pressure to near-term cash flows.

Additionally, structural anxieties regarding artificial intelligence continue to weigh on the company. Analyst discussions have increasingly focused on the risk that advanced AI tools are compressing project timelines. This shift raises long-term questions about whether generative AI will disrupt and ultimately shrink the billable hours and pricing of Accenture’s traditional IT consulting business model.

Finally, the negative momentum was exacerbated on the current trading day by major institutional revisions. Notably, analysts at Morgan Stanley significantly lowered their price target on the stock, citing ongoing market headwinds and a more cautious outlook for near-term tech spending. This downgrade, alongside a broader reassessment of the enterprise IT consulting space, has triggered capitulation among institutional holders, driving high trading volume and notable intraday volatility.

Technical Analysis of Accenture PLC (ACN)

Technically, Accenture PLC (ACN) shows a MACD (12,26,9) value of -7.785, indicating a sell signal. The RSI at 20.855 suggests sell condition and the Williams %R at 96.713 suggests oversold condition. Please monitor closely.

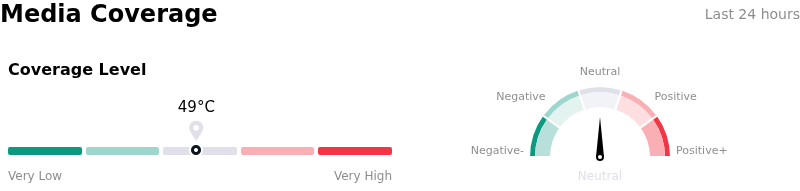

Media Coverage of Accenture PLC (ACN)

In terms of media coverage, Accenture PLC (ACN) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Accenture PLC (ACN)

Accenture PLC (ACN) is in the Software & IT Services industry. Its latest annual revenue is $69.67B, ranking 6 in the industry. The net profit is $7.68B, ranking 14 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $207.87, a high of $329.00, and a low of $135.00.

More details about Accenture PLC (ACN)

Company Specific Risks:

- Revenue Guidance Cut and Near-Term Headwinds: In its Q3 FY2026 earnings report, Accenture narrowed its full-year local-currency revenue growth guidance to 3%–4% (down from 3%–5%) and projected a weaker-than-expected Q4 revenue range of $17.75 billion to $18.40 billion. Management highlighted three ongoing growth barriers: a $100 million headwind from Middle East conflicts, persistent demand weakness in U.S. federal sales, and macro-driven client budget tightening.

- Contraction in New Bookings: Accenture's Q3 FY2026 new bookings fell 2% year-over-year to $19.32 billion, representing a steep 13% sequential drop. This contract slowdown signals that clients are taking a cautious "wait-and-see" approach to the Federal Reserve’s higher-for-longer interest rate policy, deferring major managed-service agreements into FY2027 and squeezing the near-term pipeline.

- Analyst Downgrades and AI Cannibalization Concerns: On June 22, 2026, TD Cowen downgraded ACN to Hold from Buy and slashed its price target from $258 to $150, following a similar downgrade to Market Perform by William Blair. Wall Street is increasingly concerned that Accenture’s traditional headcount-based, billable-hour model is being structurally cannibalized by rapid enterprise adoption of generative AI, which compresses consulting hours.

- Capital Allocation and Integration Risks: Alongside earnings, Accenture announced a $4.18 billion cash deal to acquire a majority stake in industrial cybersecurity firm Dragos and full ownership of runZero and NetRise. Analysts warn that this major shift from services into cybersecurity software will introduce near-term integration challenges, increase net leverage, and act as an initial drag on earnings per share.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.