Marriott International Inc Stock (MAR) Moved Down by 3.16% on Jun 22: What Signal Does It Send?

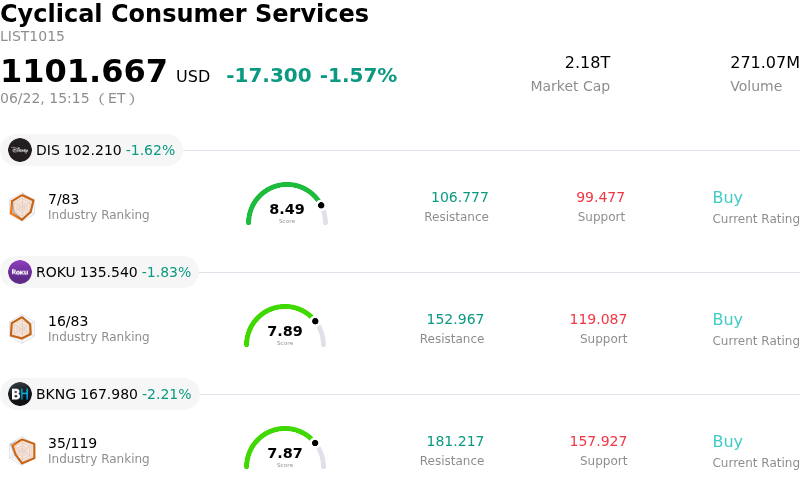

Marriott International Inc (MAR) moved down by 3.16%. The Cyclical Consumer Services sector is down by 1.57%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Walt Disney Co (DIS) down 1.63%; Roku Inc (ROKU) down 1.80%; Booking Holdings Inc (BKNG) down 2.21%.

What is driving Marriott International Inc (MAR)’s stock price down today?

Marriott International experienced a notable downward movement accompanied by significant intraday volatility, driven by a combination of macroeconomic headwinds, valuation sensitivity, and growing internal operational tensions. As trading resumed following a holiday weekend, broader market anxieties regarding persistent inflation and monetary policy weighed heavily on premium-valued equities, particularly within the consumer discretionary and travel sectors.

A primary catalyst for the downward pressure is the shifting macroeconomic landscape. Rising Treasury yields, fueled by concerns that inflation is accelerating, have intensified speculation that the Federal Reserve may implement additional interest rate hikes later this year. Higher-for-longer interest rates tend to squeeze consumer discretionary spending, casting a shadow over future travel and leisure demand. Furthermore, climbing bond yields elevate the discount rate applied to future earnings, which disproportionately impacts stocks trading at high valuation multiples. With Marriott trading at a premium price-to-earnings ratio well above its historical average, the stock proved highly vulnerable to this macro-driven contraction in valuation multiples.

Compounding these macroeconomic concerns are rising industry-specific tensions between Marriott and its franchisees. Hotel owners are aggressively advocating for a more favorable revenue-sharing model regarding the highly successful Bonvoy loyalty program, which has grown to nearly 283 million members. Franchisees argue that they are not being adequately compensated for the operational costs associated with reward-member stays, especially as Marriott’s co-branded credit card partnership fees are projected to reach substantial levels. This brewing friction introduces a risk of increased operational friction and potential margin pressure if Marriott is forced to adjust its loyalty fee structures to appease hotel operators, who form the backbone of its asset-light business model.

Additionally, overall market sentiment on the day was mixed, with expensive and high-multiple segments of the market experiencing a wave of profit-taking. Despite some positive headlines in recent weeks—such as Marriott expanding its footprint through strategic partnerships and surpassing major property-opening milestones—the lack of an immediate positive catalyst on the day left the stock exposed to broader market liquidations. As institutional investors shifted capital to manage risk amid heightened rate uncertainty, Marriott's premium valuation and reliance on resilient consumer travel spending made it a prime target for near-term de-risking, resulting in heightened price swings and a downward close.

Technical Analysis of Marriott International Inc (MAR)

Technically, Marriott International Inc (MAR) shows a MACD (12,26,9) value of 0.491, indicating a buy signal. The RSI at 62.464 suggests neutral condition and the Williams %R at 36.580 suggests buy condition. Please monitor closely.

Fundamental Analysis of Marriott International Inc (MAR)

Marriott International Inc (MAR) is in the Cyclical Consumer Services industry. Its latest annual revenue is $6.98B, ranking 21 in the industry. The net profit is $2.60B, ranking 7 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $378.88, a high of $446.00, and a low of $259.44.

More details about Marriott International Inc (MAR)

Company Specific Risks:

- Franchisee Backlash Over Bonvoy Loyalty Revenue: A coalition representing nearly 1,000 Marriott-affiliated properties has publicly protested against the economics of the Bonvoy loyalty program. Franchisees are demanding higher compensation for point-based award stays and a cut of Marriott's projected $1 billion co-branded credit card fee windfall, threatening Marriott's highly lucrative, high-margin royalty streams ($716 million last year) if the dispute forces a revenue-sharing renegotiation.

- Geopolitical Headwinds Dragging Middle East RevPAR: Ongoing conflict in the Middle East has severely disrupted regional travel, resulting in a steep 60% year-over-year decline in April Middle East RevPAR. Management anticipates a 50% regional RevPAR drop for Q2, which is projected to slice 100 to 125 basis points off Marriott's full-year global RevPAR growth.

- Underperforming World Cup Tourism Projections: Real-time booking data and third-party tourism datasets reveal that demand for the summer World Cup in North America is significantly underperforming initial forecasts, with some host-city occupancies reported as low as 15%. This directly challenges Marriott's forward guidance, which assumes the tournament will deliver a 30 to 35 basis point lift to global RevPAR.

- Premium Valuation Coupled with Weak Balance Sheet: Trading at a premium P/E ratio of over 41x, Marriott's stock is highly vulnerable to downward valuation adjustments if growth cools. This vulnerability is compounded by high leverage, marked by elevated interest expenses that climbed to $204 million in Q1, and a negative return on equity of 80.97%.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.