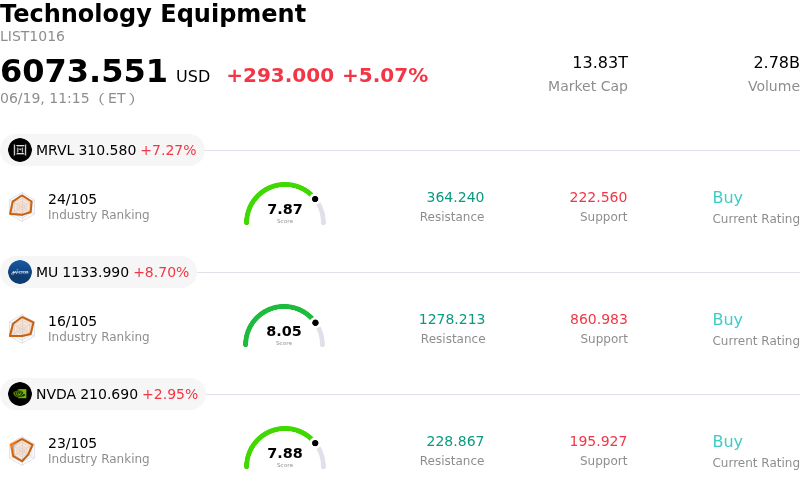

Arm Holdings PLC Stock (ARM) Moved Up by 4.91% on Jun 19: A Full Analysis

Arm Holdings PLC (ARM) moved up by 4.91%. The Technology Equipment sector is up by 5.07%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Marvell Technology Inc (MRVL) up 7.27%; Micron Technology Inc (MU) up 8.70%; NVIDIA Corp (NVDA) up 2.95%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

Arm Holdings experienced a strong upward move, continuing its recent bullish trajectory driven by growing investor confidence in its role in the next generation of artificial intelligence. The primary driver of this positive market sentiment is the structural shift toward agentic AI systems. Analysts from major financial institutions have recently highlighted that the rise of autonomous agentic AI, which requires complex multi-step orchestration and continuous inference workloads, will significantly increase the demand for central processing units. Since Arm's highly efficient CPU architectures are ideally suited for these complex coordination tasks, the shift disproportionately benefits the company's proprietary designs over traditional hardware alternatives, sparking a wave of momentum across the chip sector.

This technological optimism has been further amplified by a flurry of positive analyst updates and price target hikes. Several prominent investment banks and research firms have recently upgraded their outlooks on the stock, citing robust long-term server CPU demand and the massive potential of custom chiplet architectures. Institutions have noted that Arm’s unique licensing and royalty-based business model provides it with extensive, high-margin revenue exposure to global AI expansion without the capital-intensive manufacturing risks faced by conventional chipmakers. The broad endorsement from Wall Street has encouraged institutional rebalancing, as investors reallocate capital into high-conviction semiconductor leaders that sit at the core of the AI data center ecosystem.

Behind the technical and sentiment-driven rally lies a foundation of stellar financial performance. Arm's recent earnings reports have revealed record-breaking revenues driven by a dramatic surge in licensing activity and a doubling of its data center royalty revenues. The company's expansion into the cloud infrastructure market, bolstered by its collaboration with major technology giants to develop custom AI processors, has proven highly successful. Furthermore, the rapid transition to its advanced instruction-set architecture has allowed the firm to command higher royalty rates per chip, enabling revenue to grow faster than overall unit volumes and bolstering its high-beta momentum profile.

Despite broader macroeconomic pressures, such as the Federal Reserve’s hawkish stance on interest rates which has historically weighed on high-valuation growth stocks, the semiconductor hardware segment has demonstrated remarkable resilience. Arm has consistently outperformed its industry peers, establishing itself as a dominant force in cloud AI deployment. While some market participants remain cautious of the stock’s premium valuation multiples, the combination of concrete royalty growth, strategic hyperscaler partnerships, and the unfolding agentic AI narrative continues to fuel intense buying interest, propelling the stock upward in today's trading session.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of 5.879, indicating a buy signal. The RSI at 68.976 suggests neutral condition and the Williams %R at 8.580 suggests overbought condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $265.56, a high of $500.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- Analyst Downgrade and Sentiment Reversal: On June 18, 2026, New Street Research downgraded Arm Holdings from Buy to Neutral. This rating change reflects a major shift in institutional sentiment, warning that the stock's massive year-to-date run has pushed its price to a steep premium over its intrinsic value, triggering near-term selling pressure.

- Severe Valuation Compression and Hawkish Pressures: Following the Federal Reserve’s hawkish monetary policy updates on June 17, 2026, the company's extreme valuation—characterized by a trailing P/E ratio exceeding 490x and a forward P/E over 100x—faces intense decompression risk. This leaves Arm's high-beta shares highly volatile and vulnerable to sharp drawdowns on minor shifts in sector sentiment.

- Strategic Execution and Channel Conflict Risks: Arm's transition into direct chip manufacturing with its AGI CPU creates a potential conflict of interest that risks alienating its core intellectual property licensing base. This strategic pivot could accelerate customer defection toward open-source RISC-V and legacy x86 architectures.

- Supply Chain Bottlenecks and Executive Insider Selling: Analysts have highlighted that supply chain constraints may prevent Arm from fully meeting demand for its new custom silicon, limiting near-term revenue execution. This risk is compounded by multi-million dollar open-market share liquidations by senior executives, including the Chief Commercial Officer and Chief Accounting Officer, in late May and early June 2026.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.