Arm Holdings PLC Stock (ARM) Moved Up by 5.34% on Jun 18: A Full Analysis

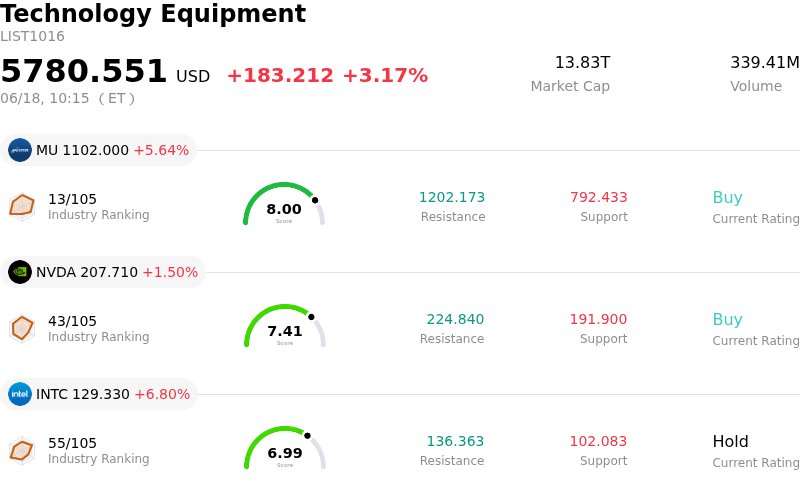

Arm Holdings PLC (ARM) moved up by 5.34%. The Technology Equipment sector is up by 3.17%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 5.64%; NVIDIA Corp (NVDA) up 1.50%; Intel Corp (INTC) up 6.80%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

The positive price movement of Arm Holdings is primarily propelled by compounding optimistic sentiment surrounding its pivotal role in the artificial intelligence sector, particularly with the rise of agentic AI. Wall Street analysts have increasingly highlighted how the transition to autonomous, agentic AI systems benefits Arm-based central processing units. Analysts argue that as complex multi-step orchestration and inference workloads multiply across enterprise deployments, the demand for highly efficient compute architecture disproportionately favors Arm’s CPU designs over traditional hardware alternatives. This structural shift has injected fresh momentum into the stock, as investors visualize Arm as a primary architect of the next phase of AI computing.

This narrative is strongly supported by the company's recent stellar financial performance. In its latest quarterly results, Arm recorded a robust double-digit increase in total revenue, driven by a sharp rise in licensing activity and a doubling of data center royalties. The company’s strategic push deeper into cloud infrastructure through its new AGI CPU—developed with Meta Platforms as a key partner—has garnered massive market interest. Customer demand for these custom, high-performance processors has skyrocketed, indicating that top cloud hyperscalers are rapidly migrating toward Arm architecture to manage AI data workloads at lower capital costs and higher power efficiency.

Complementing these fundamentals is a wave of recent bullish analyst upgrades and upward price target revisions from major financial institutions, including Mizuho, Barclays, and Bank of America. These firms have consistently pointed to accelerating server CPU demand, rising royalty rates, and Arm's expansion into custom chiplets as key drivers for long-term valuation growth. Additionally, joint initiatives, such as collaborating with Nvidia on advanced personal computer chips designed to run localized AI agents, have cemented Arm's footprint in the emerging AI PC market.

While macroeconomic factors and a hawkish stance from Federal Reserve officials have recently put pressure on broader technology and high-valuation software equities, chip hardware leaders like Arm have demonstrated significant resilience. This divergence highlights a rotation of institutional capital into high-conviction semiconductor innovators. Although high valuations and recent insider sales have sparked some near-term caution, the overwhelming secular tailwinds from agentic AI workloads and robust licensing pipelines continue to fuel the upward momentum in Arm's stock.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of 2.123, indicating a buy signal. The RSI at 66.659 suggests neutral condition and the Williams %R at 17.702 suggests overbought condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $258.98, a high of $500.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- Severe Valuation Compression Risk Under Hawkish Pressures: Following the Federal Reserve's hawkish dot-plot update on June 17, 2026, which renewed interest rate hike concerns, Arm's extreme valuation multiples have come under intense scrutiny. Trading at an exceptionally frothy trailing price-to-earnings (P/E) ratio exceeding 490x and a high beta of 3.78, the stock is highly susceptible to massive drawdowns and profit-taking on even minor shifts in broader AI-infrastructure and semiconductor sentiment.

- Ongoing FTC Antitrust Investigation: The U.S. Federal Trade Commission's (FTC) active antitrust probe into Arm’s licensing practices poses severe regulatory and headline risk. Regulators are examining whether Arm is leveraging its architectural dominance to degrade or deny design licenses to third-party chip customers as it shifts to building its own proprietary silicon, threatening its core high-margin licensing model.

- Ecosystem Friction and Competitive Defection: The company's strategic pivot into direct chip manufacturing with its 136-core AGI CPU risks alienating longstanding IP licensing customers (such as Nvidia, Qualcomm, and AWS) who now view Arm as a direct product competitor. This structural conflict of interest may accelerate licensee defection toward rival open-source architectures, such as RISC-V.

- Supply Chain and Fabrication Execution Constraints: As Arm attempts to scale its proprietary physical silicon business to hit its target of $15 billion in own-chip sales, it is exposed to manufacturing, yield, and foundry allocation risks it historically avoided under a pure-IP model. Analysts have flagged that immediate fabrication and supply bottlenecks threaten to disrupt the delivery timeline of its next-generation server processors.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.