Flex Ltd Stock (FLEX) Moved Up by 5.41% on May 29: A Full Analysis

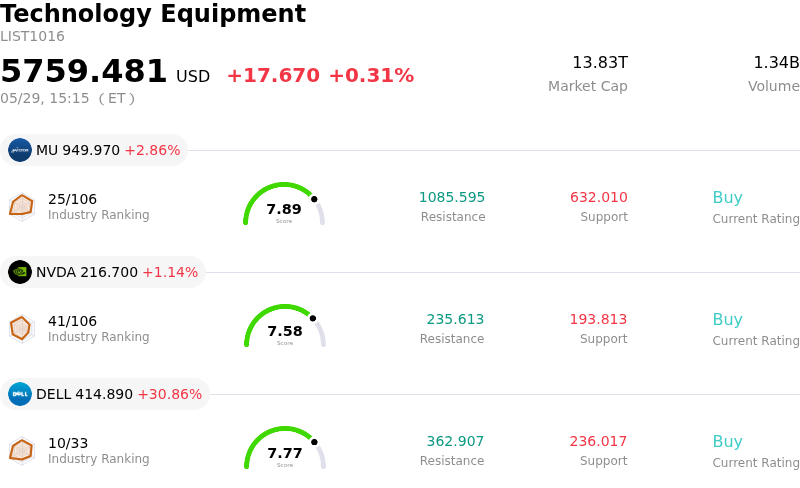

Flex Ltd (FLEX) moved up by 5.41%. The Technology Equipment sector is up by 0.31%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 2.86%; NVIDIA Corp (NVDA) up 1.07%; Dell Technologies Inc (DELL) up 30.86%.

What is driving Flex Ltd (FLEX)’s stock price up today?

Flex's stock experienced upward movement and significant intraday volatility, largely driven by recent strong financial performance and strategic corporate developments. The company reported robust fourth quarter and fiscal year 2026 results earlier this month, surpassing analyst expectations for both earnings per share and revenue. This strong performance was attributed to increased demand across its segments, particularly in the Cloud and Power Infrastructure division, and improved operational efficiency, leading to record adjusted gross and operating margins. Flex also provided an optimistic outlook for the upcoming fiscal quarter, which has contributed to positive investor sentiment.

A key factor influencing the stock's trajectory is the company's announced intention to spin off its Cloud and Power Infrastructure segment into a new independent public company. This strategic move is expected to unlock value by allowing both entities to focus on their core strengths and pursue distinct growth opportunities. The spin-off has been a significant driver for the stock's appreciation since its announcement, with some analysts highlighting the potential for the separated CPI unit to achieve a higher valuation multiple due to its faster growth and better margins.

Analyst sentiment has been mixed but generally positive, with several firms raising their price targets and maintaining "Buy" ratings, citing the successful spin-off plans and the company's focus on margin expansion. For instance, BofA Securities notably increased its price target for Flex. However, some new analyst coverage, such as a "Hold" rating initiated by Freedom Capital Markets, has introduced a note of caution regarding the stock's current valuation, suggesting it appears overvalued relative to its intrinsic value and trades at a high price-to-earnings ratio. This divergence in analyst opinion, coupled with recent strong gains, may contribute to the observed intraday volatility.

Institutional investor activity has also shown varied movements, with some firms like Legal & General Group Plc reducing their holdings in the fourth quarter of 2025, while others such as Vanguard Group Inc., State Street Corp, and Qube Research & Technologies Ltd substantially increased their stakes during the same period. Additionally, insider selling by both the CEO and COO occurred in May, although these transactions were conducted under pre-arranged trading plans, which is a common practice for executive compensation and tax obligations. Technical analysis also indicates strong sentiment supporting an overweight bias, with a breakout underway and potential for further upside, given a lack of immediate resistance levels.

Technical Analysis of Flex Ltd (FLEX)

Technically, Flex Ltd (FLEX) shows a MACD (12,26,9) value of [13.90], indicating a neutral signal. The RSI at 71.87 suggests buy condition and the Williams %R at -10.98 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Flex Ltd (FLEX)

Flex Ltd (FLEX) is in the Technology Equipment industry. Its latest annual revenue is $27.91B, ranking 2 in the industry. The net profit is $880.00M, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $150.34, a high of $180.00, and a low of $72.44.

More details about Flex Ltd (FLEX)

Company Specific Risks:

- InvestingPro analysis indicates the stock appears overvalued relative to its fair value, trading at a high P/E ratio of 62.15, with some analyst estimates suggesting the stock could be worth significantly less than its current price.

- Recent insider transactions include the CEO selling 83,500 shares on May 22, 2026, and a director selling 2,000 shares on the same date, which could be interpreted as a lack of confidence or profit-taking by key executives.

- Execution risk exists surrounding the planned spin-off of the Cloud and Power Infrastructure unit, as any delays or operational stumbles in this segment, which investors view as core to future growth, could negatively impact the stock.

- The company faces customer concentration risk within its AI data center business, with significant reliance on hyperscalers, which could lead to vulnerability if these relationships change or if vertical integration by hyperscalers increases.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.