Arm Holdings PLC Stock (ARM) Opened Up by 3.91% on May 26: A Full Analysis

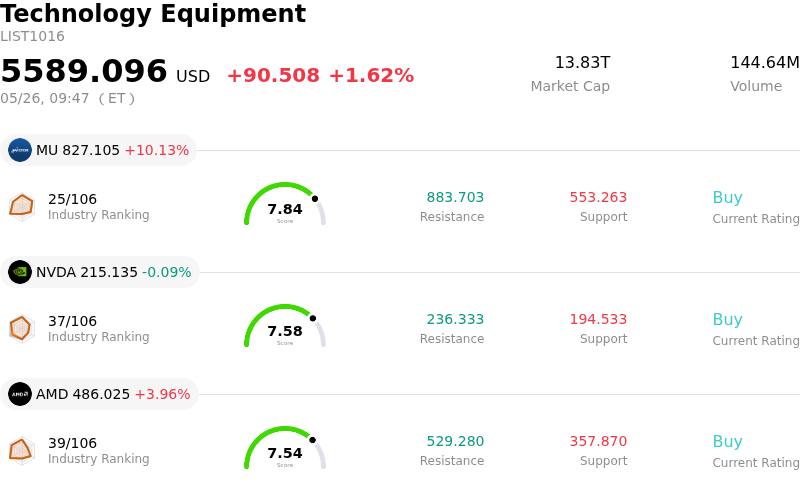

Arm Holdings PLC (ARM) opened up by 3.91%. The Technology Equipment sector is up by 1.62%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 10.13%; NVIDIA Corp (NVDA) down 0.09%; Advanced Micro Devices Inc (AMD) up 3.96%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

ARM Holdings (ARM) experienced significant upward movement, driven by several favorable factors impacting its financial outlook, industry positioning, and market sentiment.

A primary catalyst for the positive performance was the company's strong first quarter 2026 earnings report, which exceeded consensus estimates for earnings per share. Management commentary highlighted robust momentum in both licensing and royalty revenue streams. This strong financial performance is largely attributed to the widespread adoption of Arm-based architectures across critical growth markets such as cloud computing, automotive, and the Internet of Things (IoT).

The ongoing boom in artificial intelligence (AI) has significantly fueled demand for ARM's energy-efficient chip designs. ARM's architecture is increasingly becoming the preferred choice for AI applications, ranging from smart sensors to advanced AI supercomputers. Projections indicate a substantial increase in AI inference workloads, with Deloitte forecasting that these will constitute a significant portion of AI computing power, creating a substantial market opportunity that ARM is well-positioned to capture. Major players like Nvidia are also integrating Arm's architecture into their server CPUs, further solidifying ARM's critical role in the evolving AI landscape.

This optimistic outlook has been reinforced by a wave of bullish analyst sentiment. Several Wall Street firms issued "Buy" or "Outperform" ratings and notably increased their price targets for ARM in May 2026. For instance, Sanford C. Bernstein initiated coverage with an "outperform" rating and a significant price target, citing the growth in central processing unit (CPU) utilization for AI workloads. Other key firms also revised their targets upwards, reflecting confidence in ARM's long-term growth trajectory driven by its AI CPU cycle.

Furthermore, the positive momentum in ARM's stock was part of a broader rally in the semiconductor sector, particularly among AI-related companies, following strong performances in Asian markets. This reflects a generalized investor conviction in the sustained spending on AI infrastructure. The success of its majority owner, SoftBank Group, whose shares surged due to its AI involvement and substantial stake in ARM, also contributed to the positive market perception. ARM's forward guidance also reflected cautious optimism, anticipating continued revenue growth in the next quarter.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [18.09], indicating a buy signal. The RSI at 76.63 suggests buy condition and the Williams %R at -7.44 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $228.81, a high of $326.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- A potential FTC antitrust investigation into Arm's licensing practices could challenge its business model and increase regulatory risk, especially as the company expands into in-house chip development.

- Arm's strategic shift into direct chip manufacturing introduces a significant risk of channel conflict, potentially leading to reduced licensing commitments or the adoption of alternative architectures by its existing customers.

- The company has expressed concerns over securing sufficient supply chain capacity to meet the demand for new chips, which could hinder near-term growth and operational efficiency.

- Arm's high valuation, significantly above semiconductor industry averages, embeds aggressive growth expectations, making the stock vulnerable to sharp corrections if execution risks related to its strategic pivot into chipmaking materialize.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.