Fiserv Ord Shs Stock (FISV) Closed Down by 8.58% on May 5: Drivers Behind the Movement

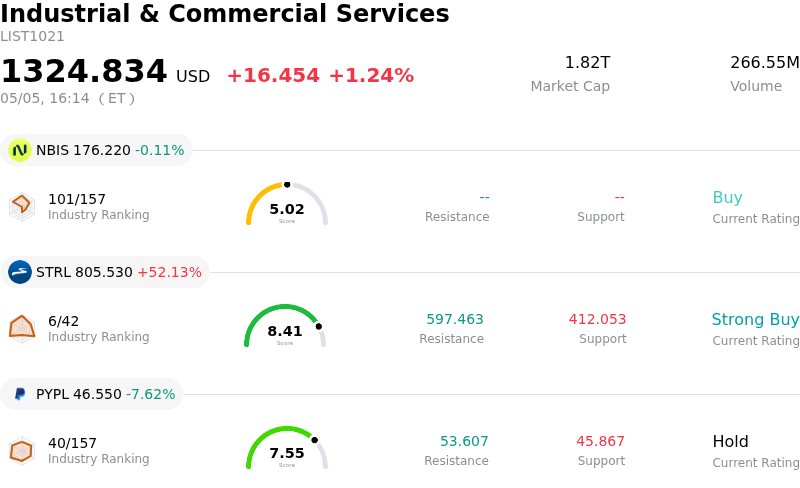

Fiserv Ord Shs (FISV) closed down by 8.58%. The Industrial & Commercial Services sector is up by 1.24%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Nebius Group NV (NBIS) down 0.11%; Sterling Infrastructure Inc (STRL) up 52.13%; PayPal Holdings Inc (PYPL) down 7.62%.

What is driving Fiserv Ord Shs (FISV)’s stock price down today?

Fiserv's stock experienced significant intraday downward volatility, declining following the release of its first-quarter 2026 financial results. Despite reporting adjusted earnings per share of $1.79, which surpassed analysts' consensus estimates, the company's revenue performance disappointed investors.

The primary drivers for the stock's negative movement were a decline in both GAAP and adjusted revenue. Fiserv reported GAAP revenue of $5.03 billion, a 2% decrease compared to the first quarter of 2025, and adjusted revenue of $4.68 billion, which fell below the consensus forecast. Organic revenue also decreased by 4% in the first quarter. This revenue shortfall was particularly evident in its Financial Solutions segment, which saw a 5% to 6% organic revenue decline, and the Merchant Solutions segment experienced flat or slight decreases in revenue.

Furthermore, operating margins compressed significantly. The adjusted operating margin was 29.7% in the first quarter of 2026, a notable decrease from 37.8% in the prior-year period. This compression was attributed to a higher expense base, including costs associated with the ongoing "One Fiserv Action Plan" transformation program and severance expenses. GAAP earnings per share also saw a substantial 29% decline compared to the previous year. Free cash flow also decreased in the quarter.

While Fiserv reaffirmed its full-year 2026 guidance for organic revenue growth and adjusted earnings per share, the market appears to have reacted negatively to the first-quarter underperformance and the implications for the company's growth trajectory, especially given that this marks the second consecutive quarter of disappointing earnings since a company "reset" in October. Analysts had already maintained a cautious stance on the stock, with several issuing price target cuts prior to the earnings release due to concerns over banking segment weakness and near-term earnings headwinds. Investors are focusing on the revenue miss and margin contraction, rather than the adjusted earnings beat. The management also indicated that the second quarter is expected to be a "trough" for revenue decline, particularly for the Financial Solutions business, which is not anticipated to recover until the second half of 2027.

Technical Analysis of Fiserv Ord Shs (FISV)

Technically, Fiserv Ord Shs (FISV) shows a MACD (12,26,9) value of [0.97], indicating a buy signal. The RSI at 60.47 suggests neutral condition and the Williams %R at -45.84 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Fiserv Ord Shs (FISV)

Fiserv Ord Shs (FISV) is in the Industrial & Commercial Services industry. Its latest annual revenue is $21.10B, ranking 4 in the industry. The net profit is $3.48B, ranking 3 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $74.30, a high of $122.34, and a low of $50.00.

More details about Fiserv Ord Shs (FISV)

Company Specific Risks:

- Fiserv's Q1 2026 results show a 4% organic revenue decline and significant adjusted operating margin compression from 37.8% to 29.7%, signaling fundamental operational weakness and increased costs associated with ongoing transformation efforts.

- Adjusted Earnings Per Share (EPS) decreased by 16% year-over-year in Q1 2026, and GAAP EPS declined by 29%, indicating a notable contraction in profitability.

- Free cash flow saw a substantial decrease, falling to $259 million from $371 million in the prior year period, limiting the company's financial flexibility.

- Multiple analysts have issued price target cuts and maintained cautious ratings due to concerns over ongoing Banking segment weakness, near-term EPS headwinds, and a lack of clear visibility on the recovery of organic growth, particularly in the Financial Services and Clover units.

Recommended Articles