Western Digital Corp Stock (WDC) Moved Up by 3.20% on Apr 17: Key Drivers Unveiled

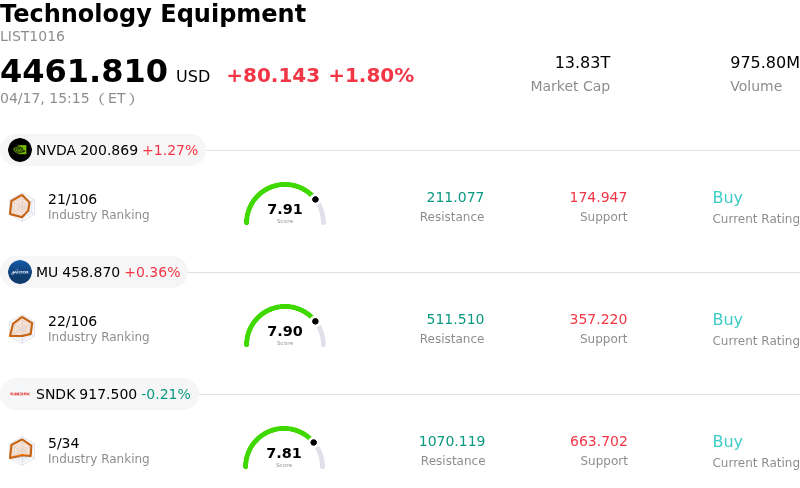

Western Digital Corp (WDC) moved up by 3.20%. The Technology Equipment sector is up by 1.80%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 1.27%; Micron Technology Inc (MU) up 0.36%; SanDisk Corporation (SNDK) down 0.21%.

What is driving Western Digital Corp (WDC)’s stock price up today?

Western Digital (WDC) experienced a notable upward movement in its share price today, influenced by a confluence of positive analyst sentiment, robust financial performance, and favorable industry dynamics.

Several prominent equity analysts recently raised their price targets for Western Digital, signaling increased confidence in the company's future prospects. Bank of America, for instance, increased its price target from $375.00 to $415.00 while maintaining a "Buy" rating, citing expectations for the company's fiscal third-quarter 2026 revenue, margins, and earnings per share to surpass current guidance. JPMorgan Chase & Co. and Cantor Fitzgerald also updated their price objectives to $400.00 and $325.00 respectively, both reiterating "Overweight" or "Buy" ratings. This collective positive re-evaluation by the analyst community likely fueled investor interest.

The company's solid financial trajectory further supported the stock's gains. Western Digital had previously reported strong fiscal second-quarter 2026 results, beating analyst expectations for both earnings per share and revenue. Looking ahead, the company provided an optimistic outlook for its fiscal third quarter of 2026, anticipating continued revenue growth and improved profitability, driven by strong data center demand and the adoption of its high-capacity drives. The upcoming Q3 FY2026 earnings announcement on April 30, 2026, with analysts projecting significant year-over-year growth, is also contributing to positive market sentiment.

Moreover, the broader hard disk drive (HDD) market is experiencing a period of significant strength, particularly in demand from hyperscale data centers and the burgeoning artificial intelligence (AI) infrastructure. Reports indicate that HDD capacity for 2026 is largely sold out, with manufacturers like Western Digital securing long-term agreements that extend into 2027 and 2028. This tight supply environment, coupled with rising demand, is leading to favorable pricing conditions and expanding gross margins for the company, driven by a strategic shift towards higher-capacity nearline drives and the adoption of UltraSMR technology. Western Digital's accelerated roadmap for advanced ePMR and HAMR drives, aimed at capacities up to 100TB by 2029, reinforces its position as a key player in meeting the escalating storage needs of the AI-driven data economy. The overall NAND flash market is also seeing strong demand and anticipated price hikes, adding to the generally positive backdrop for memory and storage providers.

Technical Analysis of Western Digital Corp (WDC)

Technically, Western Digital Corp (WDC) shows a MACD (12,26,9) value of [15.83], indicating a buy signal. The RSI at 68.47 suggests neutral condition and the Williams %R at -5.62 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Western Digital Corp (WDC)

Western Digital Corp (WDC) is in the Technology Equipment industry. Its latest annual revenue is $9.52B, ranking 8 in the industry. The net profit is $1.84B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $334.60, a high of $440.00, and a low of $92.00.

More details about Western Digital Corp (WDC)

Company Specific Risks:

- Recent analyst downgrade from a "buy" to "hold" rating by Wall Street Zen on April 12, 2026, citing valuation concerns after a significant stock price appreciation.

- Material insider selling has occurred recently, with approximately 92,795 shares valued at around $24.3 million sold by insiders, potentially signaling a lack of confidence.

- The company's core reliance on the Hard Disk Drive (HDD) business following the flash segment spin-off exposes it to substantial capital expenditure requirements and persistent market risks, including competition from Solid-State Drives (SSDs) in certain segments.

- Analyst consensus price targets, averaging between $235.58 and $285.25, are significantly below the current trading price, indicating potential overvaluation and a forecasted downside.

Recommended Articles