PDD Holdings Inc Stock (PDD) Moved Up by 4.69% on Apr 16: Facts Behind the Movement

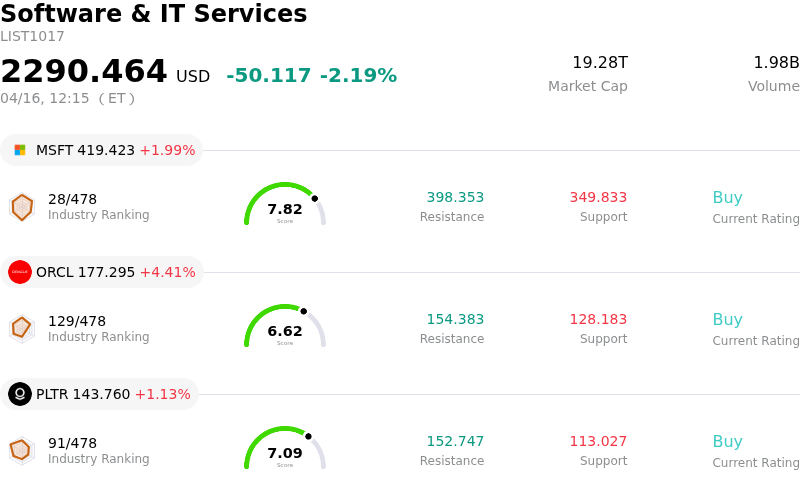

PDD Holdings Inc (PDD) moved up by 4.69%. The Software & IT Services sector is down by 2.19%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) up 1.99%; Oracle Corp (ORCL) up 4.41%; Palantir Technologies Inc (PLTR) up 1.13%.

What is driving PDD Holdings Inc (PDD)’s stock price up today?

PDD Holdings' share price experienced an upward movement, reflecting a notable rebound from recent pressures. This positive intraday shift appears to be driven by a confluence of factors, primarily a renewed focus on the company's valuation and ongoing analyst confidence, even amidst recent challenges.

The company has faced headwinds, including a miss on its fourth-quarter 2025 revenue and profit expectations, as reported in late March. Additionally, PDD Holdings, through its platforms like Pinduoduo and Temu, has been navigating intensified regulatory scrutiny in China concerning issues such as food safety, taxation, and anti-monopoly practices. Concerns have also been raised regarding the operating environment for Temu in international markets, with discussions around potential duty changes impacting its low-cost model. These factors have contributed to a period of suppressed stock performance.

However, a counter-narrative emphasizing the company's underlying value seems to be gaining traction. Despite recent setbacks, a number of analysts maintain "Buy" ratings on PDD, with several setting price targets significantly above its recent trading levels, indicating a belief in substantial future upside. Recent analysis suggests that PDD may be undervalued when assessed through discounted cash flow models, with some estimates pointing to a considerable discount relative to its intrinsic value. The company's price-to-earnings ratio is also noted as being lower than the industry average, which could make it an attractive entry point for investors seeking value.

Furthermore, institutional investor activity indicates a degree of confidence, with some firms, such as Massachusetts Financial Services Co., increasing their stake in PDD Holdings recently. This institutional backing, combined with a perception of undervaluation and a potential tempering of fears around the severity of regulatory outcomes, could be contributing to the positive sentiment. While specific new catalysts for today's rise were not immediately apparent, the collective weight of these factors suggests a market correction or a "buy the dip" mentality among investors who believe the recent negative news has been sufficiently priced into the stock, and that the long-term growth story remains intact.

Technical Analysis of PDD Holdings Inc (PDD)

Technically, PDD Holdings Inc (PDD) shows a MACD (12,26,9) value of [-0.53], indicating a neutral signal. The RSI at 51.43 suggests neutral condition and the Williams %R at -40.67 suggests oversold condition. Please monitor closely.

Fundamental Analysis of PDD Holdings Inc (PDD)

PDD Holdings Inc (PDD) is in the Software & IT Services industry. Its latest annual revenue is $62.58B, ranking 8 in the industry. The net profit is $14.40B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $142.80, a high of $198.00, and a low of $110.00.

More details about PDD Holdings Inc (PDD)

Company Specific Risks:

- Heightened and ongoing regulatory scrutiny in China, including sector-wide probes into business practices and initiated securities fraud investigations, poses a significant operational and legal threat.

- Increasing international regulatory pressures, such as the removal of duty waivers in the US and impending changes in EU duty allowances for low-value parcels, threaten Temu's cost-advantage business model and are expected to increase operational costs.

- Recent financial underperformance, evidenced by missed Q4 2025 revenue and profit estimates in late March 2026, indicates a fundamental weakness in current business operations and potential margin compression due to strategic supply chain investments.

- Intensified competitive landscape within China and broader macroeconomic uncertainties are contributing to a slowdown in growth on the domestic Pinduoduo platform, leading to increased expenses for merchant support and subsidies that pressure profitability.

Company Specific Risks:

- Heightened and ongoing regulatory scrutiny in China, including sector-wide probes into business practices and initiated securities fraud investigations, poses a significant operational and legal threat.

- Increasing international regulatory pressures, such as the removal of duty waivers in the US and impending changes in EU duty allowances for low-value parcels, threaten Temu's cost-advantage business model and are expected to increase operational costs.

- Recent financial underperformance, evidenced by missed Q4 2025 revenue and profit estimates in late March 2026, indicates a fundamental weakness in current business operations and potential margin compression due to strategic supply chain investments.

- Intensified competitive landscape within China and broader macroeconomic uncertainties are contributing to a slowdown in growth on the domestic Pinduoduo platform, leading to increased expenses for merchant support and subsidies that pressure profitability.

Recommended Articles