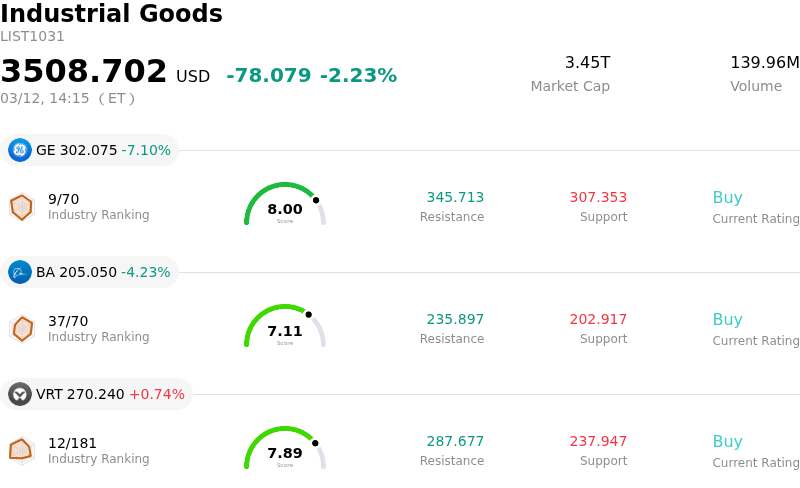

Parker-Hannifin Corp Stock (PH) Moved Down by 3.79% on Mar 12: Facts Behind the Movement

Parker-Hannifin Corp (PH) moved down by 3.79%. The Industrial Goods sector is down by 2.23%. The company underperformed the industry. Top 3 stocks by turnover in the sector: General Electric Co (GE) down 7.10%; Boeing Co (BA) down 4.23%; Vertiv Holdings Co (VRT) up 0.74%.

What is driving Parker-Hannifin Corp (PH)’s stock price down today?

PH experienced a decline in its share price today, likely influenced by a confluence of macroeconomic factors and ongoing considerations related to a recent acquisition. While the company's financial fundamentals and industry outlook remain largely positive, broader market sentiment appears to have played a significant role.

Globally, March 12, 2026, saw a retreat in equities in some markets due to a resurgence in global crude oil prices. This increase was attributed to an escalation in geopolitical tensions, specifically intensified attacks in the Strait of Hormuz. Such events typically trigger widespread inflation concerns, dampen investor risk appetite, and raise the specter of potential interest rate hikes, all of which can exert downward pressure on equity markets, including fundamentally sound companies like Parker Hannifin. Additionally, geopolitical friction directly threatens global supply chains, a concern for industrial manufacturers.

From a company-specific perspective, Parker Hannifin has generally received strong analyst ratings, with a consensus "Buy" and upward revisions to fiscal year 2026 earnings guidance, driven by robust aerospace demand and constructive trends in manufacturing. However, the company's significant acquisition of Filtration Group Corporation for $9.25 billion, announced in November 2025, presents a mixed picture. While expected to be accretive to growth and earnings, it also "meaningfully increases leverage" and elevates the company's "risk profile" compared to peers. The potential for integration challenges or increased financial risk associated with this large debt-financed acquisition could be contributing to investor caution, especially during periods of market uncertainty. Furthermore, some analysts, such as Stifel on March 5, 2026, had reiterated a "Hold" rating, noting that the stock appeared overvalued against their fair value assessment, which could have prompted some selling pressure.

Therefore, the downward movement can be attributed to the impact of heightened geopolitical risks on overall market sentiment, coupled with lingering concerns about the leverage and integration risks stemming from the Filtration Group acquisition, despite the company's otherwise strong financial performance and positive long-term outlook.

Technical Analysis of Parker-Hannifin Corp (PH)

Technically, Parker-Hannifin Corp (PH) shows a MACD (12,26,9) value of [7.27], indicating a neutral signal. The RSI at 40.88 suggests neutral condition and the Williams %R at -70.01 suggests oversold condition. Please monitor closely.

Media Coverage of Parker-Hannifin Corp (PH)

In terms of media coverage, Parker-Hannifin Corp (PH) shows a coverage score of 36, indicating a low level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Parker-Hannifin Corp (PH)

Parker-Hannifin Corp (PH) is in the Industrial Goods industry. Its latest annual revenue is $19.85B, ranking 9 in the industry. The net profit is $3.53B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1024.16, a high of $1168.00, and a low of $618.44.

More details about Parker-Hannifin Corp (PH)

Company Specific Risks:

- Significant insider selling by multiple high-ranking officers in February 2026, including the COO, CFO, and VPs, suggests a potential lack of confidence in the company's near-term outlook, with over $12 million in shares sold over the last 90 days.

- Several institutional investors, such as Bank of Montreal Can and South Dakota Investment Council, reduced their holdings in Parker-Hannifin during Q3 2025, as reported in March 2026 filings, indicating some institutional caution.

- Despite an upgraded fiscal 2026 earnings outlook, the company faces risks from rising capital expenditure and restructuring activities which could make free cash flow less predictable.

- Parker-Hannifin's increased reliance on its aerospace segment and the successful integration of recent acquisitions introduce execution risks, as any stumble in these areas could pressure margins, especially while offsetting sluggish core industrial demand.