Arm Holdings PLC Stock Moved Up by 3.47% on Feb 25: What Investors Need To Know

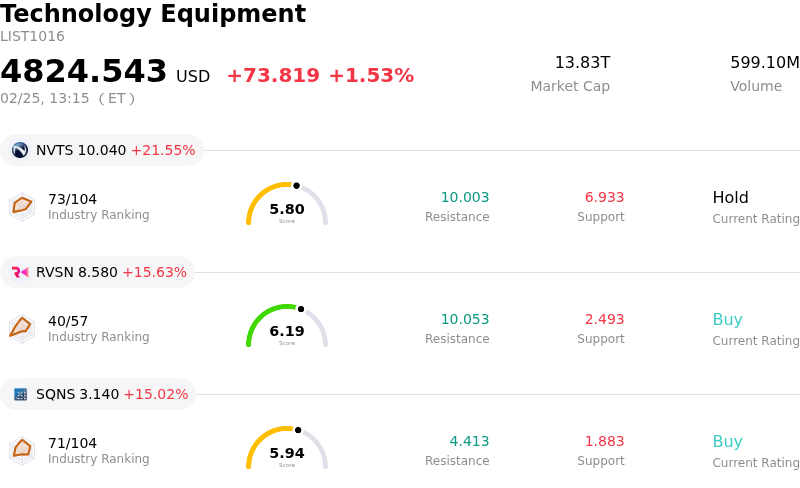

Arm Holdings PLC (ARM) moved up by 3.47%. The Technology Equipment industry is up by 1.53%. The company outperformed the industry. Top 3 gainers of the industry: Navitas Semiconductor Corp (NVTS) up 21.55%; Rail Vision Ltd (RVSN) up 15.63%; Sequans Communications SA (SQNS) up 15.02%.

Arm Holdings experienced an upward movement in its stock today, driven by a confluence of strong industry tailwinds and positive analyst sentiment. A primary catalyst appears to be the company's robust positioning within the expanding artificial intelligence sector, particularly evidenced by a reported doubling of data-center royalty revenue in the prior quarter. This growth is significantly fueled by the increasing adoption of Arm-based Graviton processors by major cloud providers for AI infrastructure, with expectations that AI inference will continue to drive demand for central processing units.

Adding to this optimistic outlook, reports indicate a strategic expansion into the personal computer market. Several prominent PC manufacturers are reportedly collaborating on laptops featuring Arm-based Nvidia-Mediatek system-on-chips, which are slated for release later in the year. This development suggests a potential increase in Arm's market share in the PC segment.

Analyst upgrades further bolstered investor confidence. A notable financial institution recently raised its price target for Arm, citing the company's increasing potential to capture a greater share of the AI inference market and the rising importance of CPUs in data center operations. Another analyst firm also upgraded the stock to a positive rating, underscoring Arm's ongoing initiatives in artificial intelligence.

The company's recent financial performance also contributes to the positive sentiment. Arm reported a solid fiscal third quarter, marking its fourth consecutive quarter of substantial revenue, with both royalty and licensing revenues showing significant increases across various segments including smartphones, data centers, and automotive applications. This broad-based growth highlights strong fundamental execution.

Despite these positive drivers, some technical analysis suggests the stock might be in overbought territory, indicating a possibility of short-term consolidation or a pullback. However, the overarching market sentiment remains confident in Arm's strategic long-term trajectory within the AI ecosystem. Furthermore, a newly announced industry consortium backed by Arm aims to foster collaboration and innovation within the Arm software ecosystem, particularly for modern computing and AI applications, which could support future growth.

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [2.30], indicating a buy signal. The RSI at 62.59 suggests neutral condition and the Williams %R at -10.36 suggests oversold condition. Please monitor closely.

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is 4.01B, ranking 26 in the industry. The net profit is 792.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 145.79, a high of 201.00, and a low of 81.78.

Company Specific Risks:

- Persistent investor concern over the company's near-term growth outlook stems from conservative guidance issued earlier in February, which, despite a recent earnings beat, only modestly exceeded expectations and failed to meaningfully impress the market or justify current valuation.

- Multiple institutional analyst downgrades, including "Sell" ratings from Goldman Sachs and Mizuho Securities in December 2025 and a "Neutral" rating from BofA Securities in January 2026, reflect ongoing skepticism regarding Arm's ability to significantly leverage the artificial intelligence (AI) cycle and concerns about its business model transition.

- The company faces challenges in its evolving business model and limited direct positioning to fully capture the upside from expanding AI infrastructure spending compared to other semiconductor entities, contributing to elevated valuation concerns.

- Geopolitical risks, particularly China's advancements toward semiconductor self-sufficiency, raise questions about Arm's long-term competitive standing and intensify concerns regarding its customer and geographic concentration in the Chinese market.