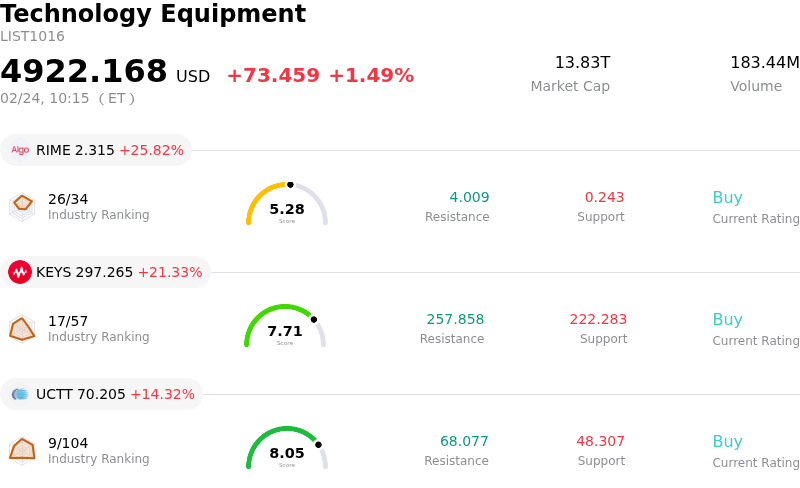

Arm Holdings PLC Stock Moved Up by 4.40% on Feb 24: Key Drivers Unveiled

Arm Holdings PLC (ARM) moved up by 4.40%. The Technology Equipment industry is up by 1.49%. The company outperformed the industry. Top 3 gainers of the industry: Algorhythm Holdings Inc (RIME) up 25.82%; Keysight Technologies Inc (KEYS) up 21.33%; Ultra Clean Holdings Inc (UCTT) up 14.32%.

ARM Holdings (ARM) experienced an upward movement in its stock price, driven by a confluence of favorable factors spanning financial performance, strategic market expansion, and positive analyst sentiment within the booming artificial intelligence (AI) and semiconductor industries.

A significant catalyst for the positive sentiment is the company's robust performance in its fiscal third quarter of 2026. ARM reported strong year-over-year growth in both royalties and licensing revenue, exceeding market expectations. This marks the company's fourth consecutive quarter of over a billion dollars in revenue. A key highlight from these results is the substantial increase in data center royalty revenue, which has more than doubled compared to the previous year. This underscores ARM's successful penetration and growing importance in the high-growth data center segment, increasingly fueled by AI workloads.

The company's strategic focus on AI and its expanding role in data centers are proving to be powerful drivers. ARM's CEO has indicated that the data center segment is rapidly becoming its primary revenue source, poised to surpass mobile in the near future. The company's architecture is critical for efficient, distributed AI computing across cloud, edge, and physical AI systems, leveraging its performance-per-watt advantage. ARM now commands a significant share of the hyperscale market for AI server CPUs. This strategic positioning is further bolstered by initiatives such as the expected unveiling of an in-house designed merchant CPU, which could considerably expand its addressable market.

Adding to the positive momentum are recent endorsements and upgrades from financial analysts. Several prominent firms have either raised their price targets or upgraded their ratings on ARM, acknowledging the company's strong AI initiatives and potential for increased market share in the CPU space by 2030. For instance, Susquehanna upgraded ARM to a Positive rating, emphasizing its AI advancements despite challenges in other market segments. This positive revision in analyst outlook contributes significantly to investor confidence.

Moreover, ARM's expansion into new product categories and collaborations further excites investors. NVIDIA is reportedly launching ARM-based laptop chips in the first half of 2026, signaling ARM's broadening influence beyond its traditional mobile market. The establishment of a "Physical AI" division, focused on robotics, and the increasing adoption of ARM Compute Subsystems, which lead to higher royalty rates and faster customer time-to-market, demonstrate the company's diversified growth avenues. The overall semiconductor industry environment, characterized by an AI-driven boom and projections for record sales, provides a tailwind for ARM's continued success.

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [2.04], indicating a buy signal. The RSI at 57.07 suggests neutral condition and the Williams %R at -23.06 suggests oversold condition. Please monitor closely.

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is 4.01B, ranking 26 in the industry. The net profit is 792.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 145.03, a high of 201.00, and a low of 81.78.

Company Specific Risks:

- Licensing revenue for Q3 FY26 fell short of analyst estimates, contributing to an 8% after-hours stock drop and raising concerns about potential weaker future royalties.

- Analysts have reduced price targets and downgraded the stock, with RBC Capital cutting its target to $130 from $140 and BofA downgrading to "Neutral" due to near-term smartphone unit headwinds and increased reliance on SoftBank in licensing.

- The company faces significant headwinds in the smartphone market, including increased memory costs and potential unit declines, impacting a major portion of its royalty sales.

- Increasing competitive pressure from the open-source RISC-V architecture poses a threat, as major customers like Qualcomm and Meta invest in RISC-V to potentially reduce their reliance on Arm's IP.